Nicolas Lippolis

Executive summary

This article examines how recent geopolitical tensions and volatility in global energy markets expose structural vulnerabilities in hydrocarbon-producing countries in Sub-Saharan Africa. Despite their importance in global oil and gas supply, these economies remain highly dependent on imported fossil fuels and are characterized by fragile energy infrastructure, limiting their ability to respond to external shocks.

The combination of foreign exchange constraints, rising debt burdens, and import dependence has led to recurrent fuel supply crises, undermining energy security across the region. In response, governments have prioritized investments in refining capacity and gas-to-power infrastructure, often framed within broader industrialization strategies. However, the article argues that such projects are frequently oversized and economically fragile, carrying significant fiscal risks—particularly in a context of uncertain long-term demand for fossil fuels.

The paper contends that efforts to achieve energy autonomy often rely on incomplete diagnostics. Rather than large-scale industrial projects, it proposes a two-pronged approach to resilience. In the short term, this involves diversifying suppliers, expanding strategic fuel reserves, and investing in logistics and storage infrastructure. Over the medium to long term, reducing structural vulnerability requires sustained investment in low-carbon power systems and the development of green industrial activities.

On the financing side, the article highlights the limitations of existing energy transition instruments, such as Just Energy Transition Partnerships (JETPs) and green taxonomies, which tend to prioritize discrete projects over broader economic transformation. For highly indebted countries, this approach constrains the ability to reconcile energy security with decarbonization and does not fully support industrialization ambitions.

As an alternative, the paper advocates for a more comprehensive approach to transition finance, aligned with national development strategies and supported by stronger coordination between public and private actors. National “country platforms” and strategic investment funds emerge as key tools. Initiatives such as Senegal’s sovereign fund for clean energy and the Nigeria Sovereign Investment Authority (NSIA) illustrate their potential to mobilize capital, coordinate investment, and reduce reliance on high-risk fossil fuel projects—provided adequate institutional capacity and governance are in place.

Ultimately, the article argues that the opposition between fossil fuel expansion and green transition is a false dichotomy. Building resilience requires addressing immediate vulnerabilities while simultaneously advancing low-carbon energy and industrial systems in an increasingly fragmented geopolitical environment.

1. Introduction

The closure of the Strait of Hormuz has put the spotlight on the vulnerabilities created by fossil fuel dependence.¹ The reliance on constant oil and gas trade flows leaves countries vulnerable to disruptions caused by wars, blockades, pandemics, and macroeconomic shocks. Even in countries that are largely self-sufficient in oil and gas, such as the United States, integrated international markets imply that domestic prices are influenced by trade disruptions elsewhere, limiting their degree of insulation and impacting inflation.²

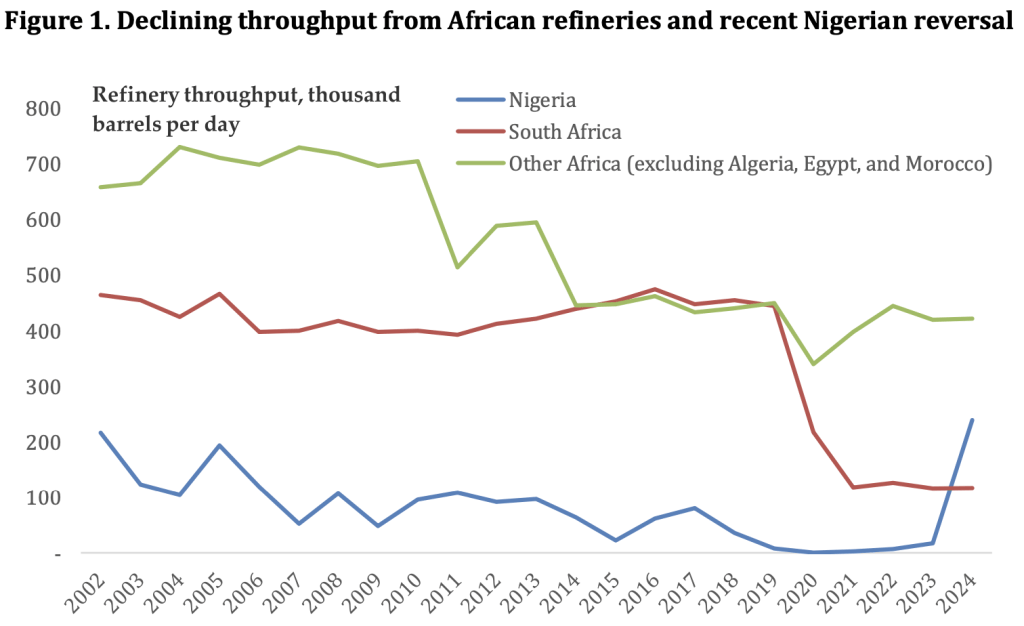

African countries have long been aware of the danger of depending on the international fossil fuels trade. Among world regions, Sub-Saharan Africa (henceforth “Africa”) hosts the largest number of countries that are highly dependent on fossil fuel imports.³ Yet, since the start of the millennium, the region has seen a decline in oil refining capacity (Figure 1), even as it experiences a population boom.⁴

Source: 2025 Energy Institute Statistical Review of World Energy

Growing dependence on fuel imports has coincided with mounting foreign exchange shortages, driven by adverse macroeconomic shocks and rising debt service burdens.⁵ These were further exacerbated by the COVID-19 pandemic and the global energy market disruptions caused by the Russia-Ukraine war. The consequences were stark: of the 36 Sub-Saharan African countries tracked by the World Bank, 15 experienced fuel shortages in 2021. This figure increased to 30 in 2022 and has remained above half the total ever since.⁶ The Iran war and its aftershocks have further aggravated this situation, leading to fuel price hikes and shortages, particularly in East Africa.⁷

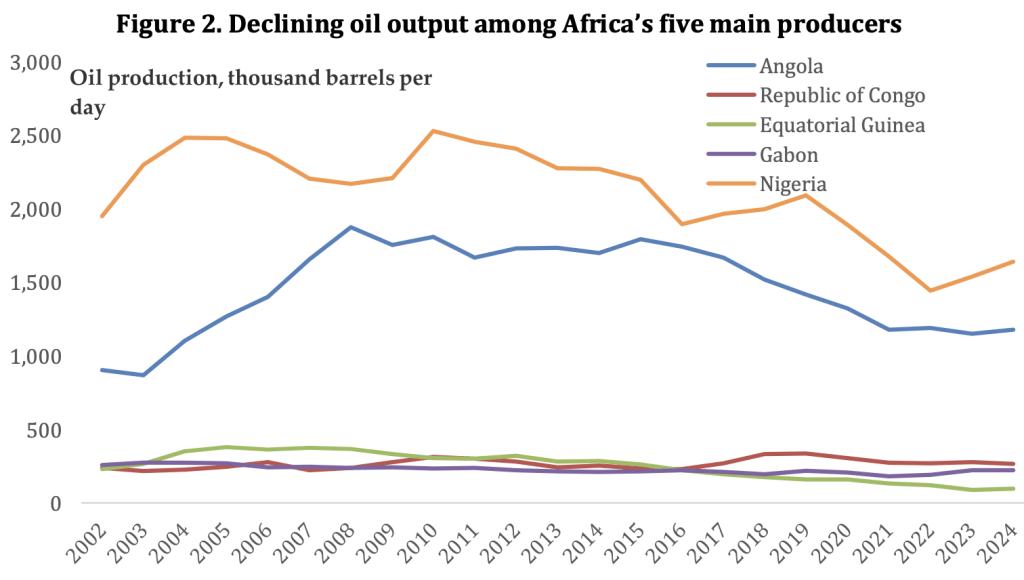

Africa’s oil exporters have also been hit by the war-induced crisis, given their dependence on fuel imports and, in many cases, the fiscal costs of fossil fuel subsidies. The paradoxical situation of exporting fossil fuels while remaining vulnerable supply disruptions has sparked renewed calls for enhancing autonomy in fossil fuel production and refining among African hydrocarbon exporters.⁸ This takes place just as a recent pickup in exploration and production investments seeks to offset the decline in oil output among the region’s major producers over the past 15 years (Figure 2).⁹ It also coincides with the coming online of Aliko Dangote’s 650,000 bpd (barrels per day) mega-refinery in Nigeria, which has rapidly increased the country’s refining capacity (Figure 1).

Source: 2025 Energy Institute Statistical Review of World Energy

The recentring of energy security reinforces earlier African efforts to reset the terms of the debate in the wake of a more fossil fuel-friendly administration in Washington. The World Bank’s adoption of an “all of the above approach” to energy finance, including natural gas and nuclear energy, echoes the Trump administration’s “energy abundance” agenda.¹⁰ U.S. Energy Secretary Chris Wright’s description of restrictions on fossil fuel financing as rooted in a “paternalistic, post-colonial attitude”,¹¹ further resonates with many Africans’ critiques of the double-standards, neglect of differentiated responsibilities, and disregard for African needs imbued in Western countries’ restrictions to fossil fuel financing.¹² Even prior to the current oil shock, analysts had pointed to the correlation between energy availability and income levels to justify the need to invest in energy generation and access, regardless of the energy source.¹³

For critics, the new focus on fossil fuels entails substantial risks. Investments in upstream oil and gas extraction could be a “risky bet” at a time when peak global oil and gas demand might be imminent.¹⁴ Were these forecasts to materialize, the balance sheets of hydrocarbon-producing states would be left with substantial “stranded assets”.¹⁵ Similarly, a recent wave of enthusiasm for natural gas-based electricity generation (“gas-to-power”) plans across Africa has raised concerns regarding their exposure to lower-than-expected gas output and the risks of prolonging the dependence of energy systems on fossil fuels just as the costs of renewable energy generation are plummeting.¹⁶

In spite of these risks, and prior to Washington’s pro-fossil fuel turn, movements to restrict international public financing for fossil fuels in Western capitals had not been accompanied by sufficient support for renewable energy.¹⁷ Even as the Iran war demonstrates the urgency of building greater resilience against fossil fuel supply shocks, and as Nigeria illustrates the benefits of domestic refining capacity, Western-led international financial institutions (IFI) continue to hold on to free-market mantras that appear increasingly out of step with the new “geoeconomic” environment. A case in point is the recent withdrawal of the World Bank’s 2026 Nigeria Development Update following severe criticism of its recommendation to resume the issuance of oil import licenses in the midst of global supply disruptions caused by the closure of the Strait of Hormuz.¹⁸

Such tone-deafness on the part of external partners could undermine mutual confidence and further cement existing – albeit deceitful – perceptions of a natural link between fossil fuels and national sovereignty. This would only exacerbate the risks created by ongoing refining and gas-to-power investments, many of which are excessively large and of doubtful economic value, as discussed below.

As blanket bans on fossil fuel financing fall out of fashion and energy security returns to the forefront of policy agendas, while renewable energy and electrification technologies – “electrotech” – become increasingly affordable,¹⁹ African oil and gas producers face strategic choices that will shape their development trajectories. However, devising more realistic approaches requires seriously grappling with the incentives and constraints pushing African governments towards sub-optimal investments in a changing (and challenging) global energy landscape.

As shown in this paper, oversized investments in fossil fuel infrastructure derive from a combination of nationalist rhetoric, energy security considerations, and industrialization ambitions in a context where development finance institutions and commercial banks have retreated from the African fossil fuel sector. In response to this, we propose a new approach for strengthening the economic resilience of African hydrocarbon producers in the face of intertwined energy security, fiscal, and climate challenges. In lieu of oversized investments in fossil fuels, we argue for a two-pronged approach to strengthening African hydrocarbon producers’ resilience by focusing both on short-term fuel security and on longer-term reduction of exposure to fossil fuel shocks.

Short-term resilience can be enhanced by improving the functioning of African fuel markets, including through diversifying sources of supply, investing in midstream infrastructure, and strengthening regional logistical coordination. Over the medium to long term, structural reductions in vulnerability will require investment not only in renewable electricity systems, but also in green industrial activities capable of providing credible alternatives to fossil fuel-led industrialization strategies. In both cases, progress will depend on proactive state action, stronger regional coordination, and sustained external financial and technical support. While these conditions have often proven difficult to achieve, the vulnerabilities exposed by recent geopolitical shocks may create greater urgency for reforms aimed at strengthening system resilience and reducing long-term dependence on fossil fuels.

The rest of this paper develops this argument in three steps. The first section examines the drivers of the recent wave of state-led investments in oil refining and gas-to-power infrastructure, showing investments aimed at supporting energy security and competitiveness may create important fiscal risks. The second section shows how, rather than large-scale investments in refining, fuel security can be improved more expeditiously by reforms to the institutional arrangements that shape fuel supply outcomes, and by upgrading regional storage and logistics infrastructure. The third section argues that avoiding the fiscal risks embedding in large fossil fuel investments will require incorporating a system-level, economic transformation perspective in existing green finance frameworks backed by IFIs and the international private sector. The final section concludes with some reflections on the need to abandon false binaries in favour of resilience-focused, development-driven strategies that integrate fossil fuel management, low-carbon investment, and institutional coordination.

2. Misdiagnosing Energy Security: The Turn to Refining and Gas-to-Power

2.1 Investments in Refining and Petrochemicals

The recent controversy around the World Bank’s Nigeria Development Update is emblematic of longstanding ideological differences on the management of Africa’s energy sector. The World Bank and the IMF attribute increasing fuel shortages in Africa to government interventions that distort the functioning of domestic energy markets, notably pervasive fuel subsidies.²⁰ On the other hand, bodies such as the African Export-Import Bank (Afreximbank), the African Energy Chamber, the African Refiners and Distributors Association, and the African Petroleum Producers’ Organization have stressed how a lack of refining capacity and low rates of utilization – themselves tied to major financing shortfalls – are the chief culprits for energy insecurity.²¹ Accordingly, recent years have seen a pickup in new refinery construction across Africa.

New refining capacity is concentrated in Nigeria and Angola, the region’s two largest oil producers. Much attention has focused on billionaire Aliko Dangote’s mammoth refinery and its dispute with the Nigeria National Petroleum Company Limited (NNPC) over access to Nigerian crude.²² Yet Angola provides a clearer illustration of the risks of overinvesting in refining. The national oil company (NOC) Sonangol is currently building three new refineries, on top of a revamp of the existing Luanda refinery. These have been slow to get off the ground: plans for a refinery in the southern city of Lobito were first mooted in the late 1990s,²³ while work on a refinery in Soyo, in the oil-producing Zaire province, officially began in late 2015.²⁴ By 2018, plans for a third refinery, in the Cabinda exclave, had been concocted.²⁵ As of January 2026, only the first phase of the 60,000-bpd Cabinda modular refinery is operational,²⁶ while the Lobito refinery is allegedly 23 percent complete,²⁷ and work on the Soyo refinery is yet to start.²⁸

Estimates based on planned refinery capacity and demand projections suggest that, if planned projects are fully implemented, total refining capacity would significantly exceed Angolan market demand.²⁹ This imbalance could create substantial fiscal burdens on the Angolan state, were the additional refineries granted subsidies similar to those extended to the Cabinda facility, including guaranteed crude supply, offtake agreements, and tax and duty incentives.³⁰ These risks are compounded by ongoing efforts to secure external financing, with Sonangol currently seeking US$ 4.8 billion from Chinese financial institutions for the 200,000-bpd Lobito refinery, though a deal has yet to be finalized.³¹

A less extreme case of state-led ambition is presented by the Hoima refinery project in Uganda. The 60,000-bpd refinery will use the crude extracted by the French major TotalEnergies and the China National Offshore Oil Corporation (CNOOC) in the Lake Albert Basin. The contract for the US$ 4 billion refinery project has reportedly been signed, though a Final Investment Decision is expected for July 2026.³² The Hoima refinery will be owned by the Emirati company Alpha MBM (60%), in partnership with the Uganda National Oil Company (UNOC) (40%).³³ Despite the lack of disclosure on financing modalities and guarantees, the project has been flagged as potentially undermining the financial viability of the East African Crude Oil Pipeline, linking production in Lake Albert to the port of Tanga in Tanzania, which only recently secured funding amid strong environmental opposition.³⁴

Beyond the objective of reducing costly fuel imports, ongoing refining projects in Africa are closely tied to ambitions to develop domestic petrochemical industries, reduce dependence on imported fertilizers, and support broader economic diversification. Uganda is again a case in point: the UNOC-owned Kabalega Industrial Park is planned to host polymer and fertilizer production.³⁵ Similarly, in Senegal, the NOC Petrosen intends to harness newly acquired hydrocarbon wealth to build a new urea plant and a second refinery.³⁶ In Angola, the long-stalled Soyo refinery project in Angola has from its inception been linked to plans for a broader petrochemicals hub, including the production of fertilizers, plastics, and synthetic fibres, as well as energy-intensive industries such as alumina refining and aluminium production.³⁷

As the largest market and largest oil and gas producer in Africa, Nigeria naturally surpasses its peers in the size of its petrochemical ambitions. The US$ 20 billion Ogidigben Gas Revolution Industrial Park, currently being developed by the China National Chemical Engineering Co (CNCEC) in partnership with the UAE’s Alpha Group, will host fertilizer, methanol, petrochemical, and aluminium plants. The complex will enjoy tax-free zone status.³⁸ Together with the petrochemical plant within the Dangote refinery complex, as well as a host of other projects, the Ogidigben Park appears poised to boost the petrochemicals industry, in line with Nigeria’s “Decade of Gas” policy.³⁹

Nigeria’s (relative) success in revamping its refining and petrochemicals sector is inseparable from the size of its oil and gas reserves and the potential market it offers. A telling counterexample again comes from Ghana, which aspires to build a “Petroleum Hub” for West Africa, including three refineries with an overall capacity of 900,000 bpd, as well as five petrochemical plants and other infrastructure, for a total cost of US$ 60 billion.⁴⁰ However, not only must this complex compete with the recently inaugurated Dangote refinery, as it seeks to serve a West African market that only consumed 800,000 bpd in 2024, while Ghana’s own crude production was at 132,000 bpd. As noted by Bright Simons, given the project’s lack of feasibility, it is most likely “a speculative attempt to grab a landbank for cheap”.⁴¹

Beyond speculative projects such as Ghana’s Petroleum Hub, the current economics of refining and petrochemicals poses real challenges to African countries’ aspirations. Stalling global demand for oil and the construction of integrated “mega-refineries” in the Middle East, China, and India have weighed on refining margins and raised the bar for new entrants to the sector.⁴² Moreover, the economics of refining favour scale, secure access to feedstock, and proximity to large consumer markets – with the exception of Nigeria, few African countries enjoy these advantages. Similar considerations apply in the petrochemicals sector, whose global demand growth has been met predominantly by large increases in production capacity in China, leaving little room for competitors.⁴³ Lacking economic competitiveness, aspiring refiners and petrochemical producers in Africa face two options: pool resources and markets or rely on state subsidies for strategic projects, with significant fiscal implications.⁴⁴

The push for increasing refining capacity in Africa responds to very real energy security needs, yet it is interlaced with industrialization ambitions and with the less salutary interests usually tied to large, state-led projects. Unfortunately, the global context is currently uninviting for investments in this sector. As a result, projects require extensive state subsidies to go forward, creating significant risk for already highly indebted sovereigns. Given the underlying motivations, however, charting an alternative course will require addressing developmental aspirations, while simultaneously finding ways to reduce African countries’ exposure to global fuel markets.

2.2 Ambitious Gas-to-Power Plans

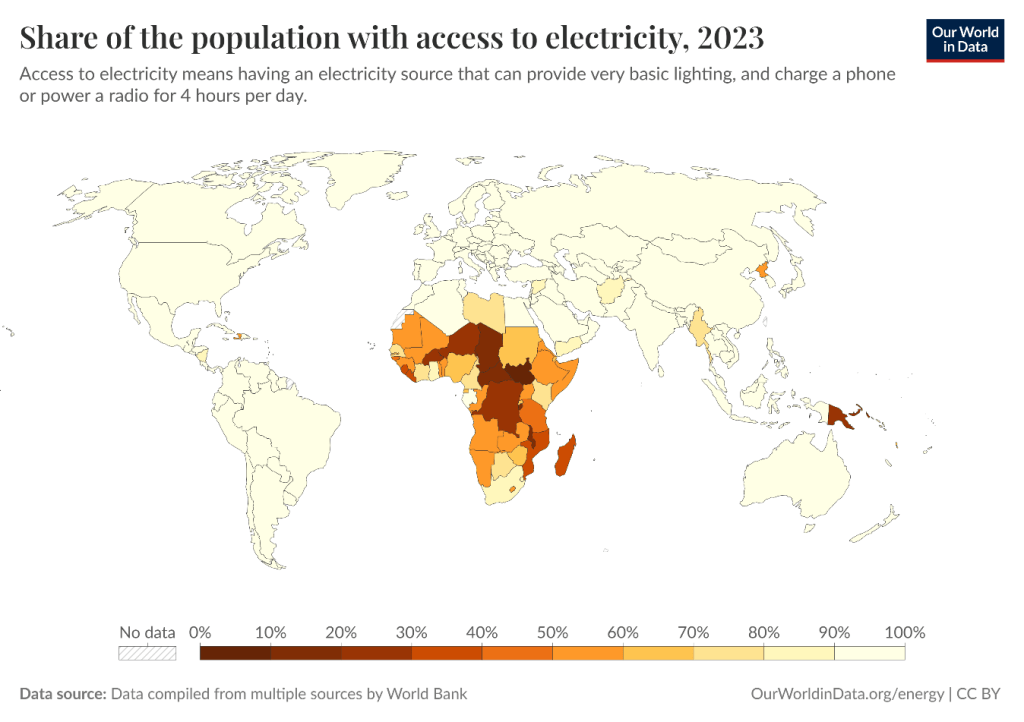

It is no secret that Africa lags other world regions in terms of energy consumption. Between 2014 and 2024, the total per capita energy supply in this region increased by an average of 1% per year, down from 1.3% in the decade 2009-2019 and below the levels seen in the emerging economies of South and South-East Asia.⁴⁵ A large part of this variation is linked to low levels of access to electricity: as of 2024, 600 million people, or 47% of the population, lacked access to electricity in sub-Saharan Africa.⁴⁶As shown by Figure 3, despite significant intra-continental variation, all of tropical Africa (i.e. excluding North Africa and South Africa) has electricity access levels well below the rest of the world.

Figure 3. Africa lags behind other world regions in access to electricity

Source: Our World in Data

While the availability of ample Chinese financing and contractors led to a boom in investments in hydropower generation in the 2000s and 2010s,⁴⁷ more recent moves to monetize associated gas in legacy producers, combined with new, non-associated gas discoveries, have spurred the development of “gas-to-power” strategies in several African countries. Gas is in fact the power generation source that has undergone the largest increase since 2014, mostly replacing the dirtier heavy fuel oil and surpassing hydropower as the main source of electricity in Africa.⁴⁸

Nigeria leads the way with its “Decade of Gas” policy, which seeks to leverage domestic gas resources for power generation, industrial feedstocks, and export revenues, as part of a broader development strategy. Similar goals are espoused by Senegal’s “Gas-to-Power Strategy”, which seeks to reduce the high electricity costs and pollution, as well as the high fiscal costs, caused by the country’s dependence on heavy fuel oil.⁴⁹ Less conspicuously, in 2025 Angola approved a Natural Gas Masterplan aimed at promoting new gas discoveries and their monetization, building a domestic gas market, and replacing diesel generation with gas in existing thermal power plants, as well as using it as a feedstock for petrochemical and other industrial sectors.⁵⁰ While the country had previously commissioned the Angola LNG (liquefied natural gas) plant and built a 750-MW combined-cycle gas-turbine power plant in Soyo, the new Masterplan represents the first comprehensive, sector-wide strategy.

Besides Nigeria, Senegal, and Angola, other current and aspiring gas producers have stated their ambition to build their gas-to-power infrastructure, including South Africa, Ghana, Tanzania, and Mozambique.⁵¹ However, the foreign companies developing African gas sectors eye the more profitable global LNG markets as their primary outlet, resulting in potentially conflicting goals. Selling to domestic markets entails significant counterparty risk, as unstable regulation can lead to tariff adjustments, payment arrears, and contract renegotiations in the region’s highly indebted states. It also requires building out domestic gas infrastructure, which might be difficult to finance due to a “chicken-and-egg-paradox”: “investors who can provide the necessary infrastructure expect guaranteed demand yet demand only grows once that infrastructure is in place”.⁵² In addition, new producers in particular might run the danger of overestimating future gas production, particularly if they disregard potential reductions in demand due to an accelerating global energy transition.⁵³

Given the risks entailed by oversized investments in gas-to-power infrastructure, analysts have stressed the need to “right-size” gas-to-power plans.⁵⁴ Unlike liquid fuels, gas-based power generation has market-ready, and often cheaper, alternatives in solar and wind power. Although gas power plants may still play a role in stabilizing electricity grids and providing baseload capacity, this does not imply that they should dominate generation mixes. Moreover, given the trade-off between greater domestic gas use and reduced export attractiveness, a more balanced strategy would limit gas investments to what is required for grid stability, while channelling revenues from LNG exports into the expansion of renewable-based power systems.

The use of fossil fuel revenues to finance low-carbon energy and economic systems has been widely advocated, but significant constraints arise in practice.⁵⁵ Chief among these are high levels of public debt, which limit governments’ ability to earmark revenues for specific investments. As discussed later in this paper, shifting towards lower-carbon power systems will therefore require both international support and greater mobilization of private capital. More fundamentally, because gas-to-power strategies are often closely tied to industrialization ambitions, such a shift will also require adaptations in international transition finance frameworks, including greater recognition of the role of energy use in supporting industrial development.⁵⁶

However, any policy frameworks must also consider the short-term needs for fuel security as countries are yet to transition to low-carbon energy systems. Advocating for large-scale decarbonization while disregarding the realities of continued fossil fuel dependence risks undermining the credibility of such advice in the eyes of policymakers facing immediate energy security constraints. In view of this, the next section examines policy options for enhancing short-term resilience to disruptions in fossil fuel imports.

3. Enhancing short-term resilience

3.1 Diversifying fuel suppliers

The choice between dependence on global fuel markets and the build-up of domestic refining capacity is often framed as one between cheaper free markets and costly protectionism. Yet this view, even when endorsed by IFIs, risks obscuring the non-competitive interests that profit from fuel trade across Africa. The link between large, commodity-trading firms, offshore financial centres, and illicit financial flows is well-documented.⁵⁷ The lack of refining capacity in Africa is in fact often attributed to the collusion between national elites given preferential access to import licenses and international, mostly Swiss- and Singapore-based, commodity traders. The political dispute between Aliko Dangote and Nigerian regulators on rules prioritizing crude supply to domestic refiners is instructive in this regard.⁵⁸

Besides reducing public revenues and encouraging corruption, elite collusion with commodity traders may also undermine energy security by hindering the adoption of more strategic and diversified sourcing strategies. In this context, the heightened fuel security concerns that currently preoccupy most African states may open windows of opportunity to dismantle trading monopolies, as moments of crisis weaken the grip of incumbent players and open space for more diversified supply arrangements.

Angola’s evolving fuel policy illustrates this dynamic, highlighting the intertwined politics of fuel trading, refining, and domestic midstream and logistics infrastructure. During the 2000s post-civil war reconstruction boom, the commodity trader Trafigura expanded its role in the Angolan fuel importation business. By the 2010s, fuel imports had become highly concentrated in joint ventures linking Trafigura to politically connected elites, including figures close to the presidency.⁵⁹ Through the Puma Energy holding company, Trafigura, Sonangol, and these elites came to dominate fuel distribution, creating a tightly controlled system spanning both imports and downstream markets. The use of complex offshore structures underscored the internationalized nature of the rent-seeking arrangements underpinning Angola’s fuel supply.⁶⁰

The post-2014 oil price downturn set in motion events that would undermine these arrangements. Faced with large amounts of debt, Sonangol struggled to honour its financing commitments with the Puma Energy partnership.⁶¹ The NOC’s financial troubles increased the frequency and intensity of the country’s periodic fuel shortages caused by the dependence on oil tankers for fuel storage.⁶² Vulnerability to maintenance disruptions and logistical delays meant that even localized issues could quickly escalate into nationwide fuel shortages.⁶³ It is during this period that plans for a major oil storage terminal were first mooted but would only come to fruition in 2025.⁶⁴

Reacting to major disruptions caused by fuel shortages – and amid a broader power reshuffle following João Lourenço’s election to the presidency in 2017 – the Angolan government moved to dismantle Trafigura’s near-monopoly on fuel imports. This opened the market to other trading houses, including Vitol, Glencore, and the French oil major Total.⁶⁵ The opening of the fuels sectors also coincided with the rekindling of refining plans, pointing to the likely role of the previous monopolies in blocking more resilient fuel policies.

The Angolan case has parallels across the region, where a small set of players often control vital fuel trading channels, in collusion with commodity traders.⁶⁶ This is particularly true in oil and gas producing countries, where these relationships tend to be deeper, more institutionalized, and embedded within broader political and financial arrangements. Strengthening energy security will necessarily involve replacing such arrangements with more open and competitive ones. However, this alone is unlikely to reduce vulnerability to fuel supply disruptions – this is where storage and logistics play a key role.

3.2 Upgrading storage and logistics

Civil society voices have been quick to point out how fossil fuels exacerbate the vulnerability to geopolitical crises and how the shift to an energy mix based on renewable energy offers the best solution.⁶⁷ However, in the short-term, this is not a luxury that governments can afford, given the pressing need to protect energy systems that are still largely fossil-based. In this context, strategic fuel stocks, in the mould of the U.S. or Chinese Strategic Petroleum Reserves, have entered the African policy agenda.

Nigeria has taken the lead with a 2025 announcement that it would create a national strategic petroleum products stockpile.⁶⁸ While other African countries have yet to follow Nigeria’s example – and Nigeria itself has yet to follow through on its announcement – policy discussions have increasingly turned to the need to expand stocks in existing storage facilities. This reflects a broader recognition of midstream infrastructure as a key enabler of fuel security.⁶⁹ Besides storage, African logistics infrastructure – including ports, pipelines, rail, trucking systems, and distribution networks – is often inefficient and dominated by a small number of players.⁷⁰ In addition, the large number of landlocked African countries means that several countries depend on a few chokepoints for their fuel supply.

The case of East Africa is particularly illustrative of the logistical difficulties in the African fuel trade. Uganda, Rwanda, and other Great Lakes countries rely on a corridor-based system linking inland markets to the ports of Mombasa and Dar es Salaam.⁷¹ Regional trade is made less efficient by the dependence on road transport, inefficient cross-border logistics, and the fragmentation of transport systems across modes and jurisdictions.⁷² Disruptions in Kenya’s pipeline system or domestic supply conditions have repeatedly generated fuel shortages across the region, with Kenyan authorities prioritizing domestic demand during crises.⁷³ Uganda, in particular, is greatly affected by these episodes, given that 90 of its fuels are imported through Kenya. In this context, Ugandan efforts to build a refinery must be seen an investment in fuel security to avoid over-dependence on its neighbour. However, such problems could be avoided if a more reliable, efficient, and rule-bound fuel trade system were in place.

More efficient sub-regional logistics systems could go a long way towards supporting resilience to external shocks to the fuel trade while disincentivizing financially perilous investments in refineries. Here, countries could draw on external risk guarantees from multilateral and bilateral development agencies, as well as institutional support, to build rule-bound, regional import, storage, and trading arrangements. Lessons can be learned from the successes and failures of previous efforts, such as the West African Gas Pipeline (WAGP) linking Nigeria, Benin, Togo, and Ghana. The Pipeline received financial guarantees from the International Finance Corporation (IFC), part of the World Bank Group, alongside broader de-risking support aimed at crowding in private investment and facilitating regional coordination. Although the WAGP has often suffered from supply disruptions, payment arrears, and underutilization,⁷⁴ it offers important lessons on how IFIs can help make cross-border infrastructure projects bankable and advance regional integration at relatively low upfront cost.

None of the actions outlined above – diversifying sourcing strategies, enlarging strategic stocks of key fuels, building regional trading arrangements, investing in midstream infrastructure – can on its own significantly reduce exposure to external fuel shocks. However, investing over US$ 100 billion in building a wave of refineries, as defended by industry advocates,⁷⁵ does not offer a good solution either. Instead, a case-by-case approach to strengthening the resilience to external supply shocks is preferable to the prestige politics of refining. The appropriate policy response depends on the nature of the constraint: where bottlenecks are logistical, targeted investments in storage, transport, and distribution are likely to yield higher returns at lower cost, whereas large-scale refining projects are justified only in a narrow set of conditions and are unlikely to be widely replicable, as illustrated by the exceptional case of the Dangote Refinery.

In practice, this points toward more incremental and system-oriented solutions. Smaller-scale or modular refining may in some cases enhance resilience, but often the more efficient path lies in upgrading existing facilities and embedding any new capacity within integrated regional markets that can ensure demand and improve viability. Ultimately, while strategies must be tailored to country-specific conditions, the current wave of supply disruptions may create an opportunity to move beyond fragmented national approaches, as shared vulnerability strengthens the case for deeper regional coordination in fuel supply systems. This can help increase short-term resilience while countries gradually build low-carbon energy and economic systems that reduce their structural vulnerability to global fossil fuel flows.

4. Financing low-carbon energy systems

4.1 Towards a broader conception of transition finance

The recent uptake in refining and gas-to-power investments in Africa is driven by both energy security and industrialization aspirations. Besides their role in granting countries greater autonomy from global fuel markets, increased refining and gas generation capacity are expected to enable the flourishing of domestic petrochemical industries, reduce domestic fuel and electricity costs, and generate new sources of employment and foreign exchange. However, these aspirations have frequently led to oversized investments, entailing fiscal risks and entrenching fossil fuel dependence.

The restrictions on financing for downstream fossil fuel investments bemoaned by African policymakers do little to reduce these (legitimate) aspirations. Restrictions are also ineffective in their own terms, as ongoing refinery projects have secured financing from either Chinese, Gulf, or African sources.⁷⁶ While this is not in itself a harmful development, it can become one if financing conditions involve government guarantees, exorbitant interest rates, or more opaque lending conditions than those of “traditional” multilateral or bilateral official donors.

As argued here, an adequate response to this conundrum is not to provide cheaper finance to uneconomical refining or thermal power plant projects but to strengthen short-term resilience to fossil fuel shocks while investing in low-carbon energy system restructuring. However, existing sustainable and transition finance frameworks remain poorly suited to this task, as most green and sustainable finance instruments continue to prioritize clearly defined, project-based investments in renewable energy and energy efficiency rather than systemwide transformation.

This limitation is reflected in the design of sustainable finance taxonomies, which are currently one of the most popular instruments for financing climate-aligned investments.⁷⁷ The European Union and China have been the pioneers in the global spread of taxonomies. The European approach, based on detailed technical screening criteria and emissions thresholds, is well suited to classifying end-state environmental performance, but less so to guiding structural transformation in developing economies. By contrast, China’s green finance framework has historically taken a more strategic approach, identifying priority sectors aligned with national development objectives.⁷⁸ While these outcomes cannot be attributed to financial frameworks alone, they are consistent with a broader model in which green finance, industrial policy, and state coordination are closely aligned, as illustrated by China’s emergence as a dominant producer of clean energy technologies. This comparison highlights the importance of aligning financial frameworks with broader development strategies, rather than treating sustainability as a purely technical classification exercise.

For Africa’s highly indebted economies, which continue to depend on external financial flows, moving towards a more encompassing view of transition finance will require reforms in IFI approaches. An important case is that of the World Bank’s and African Development Bank’s Mission 300 (m300) program, which aims to connect 300 million Africans to electricity by 2030. M300 brings a welcome combination of investments in on-grid and off-grid solutions across the entire region; however, it lacks a focus on industrial uses of energy, which might fail to satisfy African governments’ industrializing ambitions. In response, the program could introduce modalities targeting electrification around productive-use clusters, such as agro-processing zones, cold chains, mining-service towns, industrial parks, and commercial corridors.⁷⁹ This could be complemented by industrial finance for these activities directly. In this way, m300 missions could directly incorporate productive-use windows, making the program a more attractive counterweight to fossil fuel-based industrialization plans.

Recent innovations in debt-for-climate and debt-for-nature swaps – now often reframed as “debt-for-development swaps” – offer further opportunities to rethink transition finance frameworks. Compared to earlier models, these instruments have moved away from strict earmarking of proceeds, as donors increasingly recognize that more flexible arrangements, combined with sound public financial management, can reduce transaction costs and improve long-term outcomes.⁸⁰ Revamped debt-for-development frameworks could provide an additional tool for financially constrained African sovereigns to invest in energy security, including through improvements to fuel logistics infrastructure and the gradual expansion of low-carbon energy and industrial systems.

Even as emerging transition finance modalities offer opportunities to rethink energy sector investment, it is important to draw lessons from existing experiences. The key precedent is provided by Just Energy Transition Partnerships (JETPs), the flagship climate finance initiative promoted by Western countries. By most accounts, JETPs have fallen short of expectations, reflecting both the limited scale and concessionality of the most debt-based financing mobilized.⁸¹ However, their limitations cannot be attributed solely to shortcomings in external support, as domestic vested interests, bureaucratic fragmentation, and political short-termism have also weighed on progress in early adopters such as Indonesia and South Africa.⁸² As a result, only a small fraction of committed financing has been mobilized, eroding trust in international climate and transition finance initiatives.

These limitations do not undermine the case for large-scale, coordinated transition financing, but rather point to the need for new institutional architectures. The experience of JETPs underscores the importance of stronger domestic ownership, more flexible financing structures, and mechanisms capable of coordinating investments across sectors and actors. In response, growing attention has turned to country platforms and strategic investment funds, which aim to align public and private finance around nationally defined priorities while addressing the political and institutional constraints that have hindered earlier initiatives.

4.2 Aligning finance and strategy: country platforms and strategic investment funds

Even reformed transition finance instruments cannot serve Africa’s energy and developments needs unless accompanied by enabling frameworks at the country level. African governments have been relatively slow to mobilize green and climate finance due to limited familiarity with available instruments, as well as high transaction costs, demanding project requirements, and the need for complex intra-governmental coordination.⁸³ In addition, the large number of highly indebted states in the region might baulk at contracting foreign currency loans. Not only might they further aggravate debt woes – assuming investors are even interested in the first place – as green financial instruments will be ineffective in the absence of adequate debt management frameworks and credible fiscal policy regimes. It is therefore imperative to match any green financing with capacity-building and the establishment of a concerted, government-wide green industrialization strategy.⁸⁴

A prominent response has been the strengthening of “country platforms”: nationally led coordination frameworks that align governments with external financiers to mobilize and sequence finance at scale for development and climate objectives.⁸⁵ While JETPs represent the most visible examples of such platforms, other experiences, such as Brazil’s Climate and Ecological Transformation Platform (BIP) and Egypt’s Nexus of Water, Food and Energy (NWFE) platform, are often regarded as more successful..⁸⁶

Comparative evidence suggests that country platforms succeed when supported by strong coordination within government, a clear mandate from political leadership, and close alignment with national development strategies and fiscal frameworks. In Brazil and Egypt, these conditions were reinforced by the presence of capable domestic institutions playing a central coordinating role, namely Brazil’s National Development Bank (BNDES) and Egypt’s Ministry of International Cooperation.⁸⁷ This suggests that mobilizing public and private finance to improve energy system resilience in Africa will require activating similar “pockets of bureaucratic effectiveness” to compensate for the shortcomings in the regular state apparatus.⁸⁸

Emerging experiences among African hydrocarbon producers can offer useful learnings on how to structure and deploy pockets of bureaucratic effectiveness to pursue energy system transformation. In particular, strategic investment funds (SIFs) can play an important role in anchoring both external and private sector investments. These funds function as state-backed financial institutions designed to crowd in private capital and coordinate investment flows toward strategic sectors, often operating with greater flexibility than traditional public budgeting processes.⁸⁹ While incipient, early experiences with climate finance mobilization by SIFs could offer instructive lessons on their role in strengthening national policy coordination.

An important case is that of Senegal, which has also struggled to make progress with its JETP. The government has recently assigned responsibility for the implementation of €2.5 billion in JETP-derived renewable energy and energy efficiency projects to the Renewable Energy & Energy Efficiency Fund (REEF), hosted by FONSIS (Sovereign Fund for Strategic Investments).⁹⁰ Within the REEF, a new “Green Energy Fund Senegal” has been created with the aim of mobilizing up to CFA 135 billion (around US$ 240 million) to “make equity investments in renewable energy and energy efficiency projects initiated by private companies in Senegal or the sub-region.”⁹¹ Although it is too early to properly evaluate Senegal’s experience, the assignment of responsibilities to the country’s generally well-regarded SIF suggests that such arrangements could offer a promising pathway aligning private and official finance with energy system resilience.

The potential of SIFs in African hydrocarbon producers can also be glimpsed from the experience of the Nigeria Sovereign Investment Authority (NSIA), generally regarded as the best performing fund in Africa. Within NSIA, the Nigeria Infrastructure Fund has successfully mobilized over US 1 billion co-investment capital and delivered infrastructure projects in sectors such as energy, transport, and healthcare, illustrating how well-governed public investment vehicles can crowd in private capital and anchor long-term development investments.⁹² More recently, NSIA has partnered with Nigeria’s National Council on Climate Change, as well as several foreign institutions, in launching several renewable energy funds and climate finance vehicles, including a Climate Investment Platform and recently announced plans to establish a US$ 2 billion National Climate Change Fund.⁹³

There is still limited evidence on the success of African SIFs in catalysing low-carbon energy investments, given that most experiences are in their early stages. Existing policy studies on the topic focus either on descriptions of, and the rationale for SIFs;⁹⁴ or discuss how they could be deployed more effectively for the low-carbon transition.⁹⁵ Missing from existing discussions is a critical evaluation of experiences with the use of SIFs to support clean energy investments. For instance, one outstanding question is what SIFs can do to mobilize more financing from sovereign wealth funds.⁹⁶ Yet while prescriptive studies have an important role to play in identifying best practices for SIFs, the design of more actionable strategies will require grappling with the political strategies required to create and sustain “pockets of bureaucratic effectiveness” within the state apparatus.⁹⁷

Despite the challenges of establishing them and preserving their technocratic integrity, robust SIFs can, once in place, help countries tap into climate and transition finance initiatives and provide more attractive alternatives to fossil fuel investments. Incipient experiences in Senegal and Nigeria also suggest that these funds can help catalyse private investments, which is particularly important in view of the fiscal constraints faced by sovereigns. In addition, they can support the strategic allocation of capital between short- and long-term priorities, including investments in midstream oil and gas infrastructure where appropriate for ensuring energy security.

5. Conclusion: beyond false dichotomies in energy transitions

Increasing geopolitical instability and the erosion of the “liberal international order” has heralded a new era of “geoeconomics”, where states combine economic leverage with traditional foreign policy tools in power competition.⁹⁸ In this context, repeated foreign policy crises are spreading awareness of the vulnerabilities created by continued reliance on internationally traded fossil fuels. Even economies that are largely self-sufficient in energy, such as the United States, cannot fully insulate themselves from global energy crises, given the financial and trade integration of global oil and gas markets.

Yet the risks posed by volatile energy markets are particularly acute in Africa, given the continent’s heavy dependence on fossil fuel imports. While oil and gas producers might benefit in the short run from oil price spikes induced by foreign policy crises, national security and economic considerations might well accelerate the transition away from fossil fuels across the world, as awareness of the risks of continued fossil fuel dependence spreads.⁹⁹ Shrinking global markets, unfavourable economics for refining, and concerns with natural gas provision create risks for state-led investments in oil and gas. Although Africa’s an immediate phase-out of fossil fuels is unrealistic, not least because of differentiated historic responsibilities, any ongoing investments must be planned prudently, while ensuring that low-carbon alternatives are developed.

At the same time, recent disruptions have underscored that energy vulnerability in Africa is not only a function of import dependence, but also of how fuel systems are organized. Across much of the continent, exposure to external shocks is amplified by bottlenecks in storage, transport, and regional coordination, as well as by the concentration of trading power in a limited number of actors. As a result, the choice between reliance on global fuel markets and the construction of domestic refining capacity presents a false dichotomy. In many cases, targeted investments in midstream infrastructure, strategic storage, and regional logistics networks would deliver greater resilience at lower cost than large-scale refining projects, while avoiding the fiscal risks associated with overcapacity and subsidized operations.

Framing energy strategies around system resilience and development rather than a simple binary between “dirty” and “clean” investments has important implications for how transition finance is conceived. International climate and sustainable finance initiatives that seek to incentivize the adoption of low-carbon development trajectories must acknowledge African countries’ industrializing aspirations and broaden their scope beyond narrowly defined green categories. At the same time, African governments must abandon the prestige politics of refining and gas-to-power investments and adopt more granular and cost-effective approaches to supporting resilience.

Doing so will depend not only on mobilizing greater volumes of capital, but also on developing institutional arrangements that can coordinate investments across sectors and time horizons. Country platforms and strategic investment funds offer promising avenues in this regard, particularly when anchored in capable domestic institutions and aligned with national development strategies. However, their effectiveness ultimately hinges on the ability to overcome domestic political economy constraints and to translate coordination into sustained investment flows.

In a context of persistent geopolitical fragmentation, African governments face the dual challenge of managing immediate energy security risks while preparing for a more uncertain and potentially contracting global market for fossil fuels. Navigating this transition will require moving beyond simplistic oppositions between fossil fuels and renewables, or between state-led and market-based approaches and instead adopting a more integrated view of energy systems, finance, and development. Building resilient, low-carbon energy systems is therefore not simply a matter of scaling up investment in new technologies, but of rethinking how energy systems are organized, financed, and governed in an increasingly unstable global environment.

Notes and references

1. The author would like to thank the following for feedback on earlier drafts of this paper: Katie Auth, Papa Daouda Diene,Patrick Heller, Peter Lindner, Amir Shafaie, Zainab Usman, Olivier Vallée, and Harry Verhoeven.

2. Debbie Carlson, “White House Worries as Gas Prices Jump amid Ongoing US-Israel War on Iran,” The Guardian, March 8, 2026.

3. Greg Muttitt and Harald Winkler, Transitioning away from Fossil Fuels in a Just, Orderly and Equitable Manner: A Quantitative Overview of Countries’ Fossil Fuel Dependence and Opportunities for Flourishing Post-Fossil Economies, PRISM Working Paper 2026-2 (Cape Town: Policy Research on International Services and Manufacturing, University of Cape Town, 2026).

4. Agence Française de Développement, “Sub-Saharan Africa Faces Persistent Demographic Challenges,” AFD, January 12, 2026., https://www.afd.fr/en/news/sub-saharan-africa-faces-persistent-demographic-challenges

5. International Monetary Fund, Regional Economic Outlook: Sub-Saharan Africa: Holding Steady (IMF, October 2025).

6. World Bank, Global Fuel Subsidies and Price Control Measures Database, May 28, 2025, https://datacatalog.worldbank.org/search/dataset/0066833/Global-Fuel-Subsidies-and-Price-Control-Measures-Database.

7. Nesrine Malik, “How the US-Israel war on Iran is affecting African economies”, The Guardian, April 15, 2026.

8. African Energy Chamber, “Africa Must ‘Refine, Baby Refine’ as Global Supply Disruptions Expose Need for Downstream Expansion,” April 13, 2026, https://energychamber.org/african-energy-chamber-africa-must-refine-baby-refine-as-global-supply-disruptions-expose-need-for-downstream-expansion/.

9. African Energy Chamber, “Africa’s Major Upstream Projects Set Stage for 2026 Investment Surge,” November 6, 2025, https://energychamber.org/africas-major-upstream-projects-set-stage-for-2026-investment-surge/.

10. Reuters, “World Bank’s Banga Seeks Board Approval for ‘All of the Above’ Energy Strategy,” April 16, 2025, https://www.reuters.com/business/energy/world-banks-banga-seeks-board-approval-all-above-energy-strategy-2025-04-16/

11. African Energy Chamber, “AEC Endorses U.S. Energy Secretary Chris Wright’s Support for African Energy Independence,” March 8, 2025, https://energychamber.org/aec-endorses-u-s-energy-secretary-chris-wrights-support-for-african-energy-independence/.

12. Yemi Osinbajo, “The Divestment Delusion: Why Banning Fossil Fuel Investments Would Crush Africa,” Foreign Affairs, August 31, 2021, https://www.foreignaffairs.com/articles/africa/2021-08-31/divestment-delusion.

13. Vijaya Ramachandran, “The World Bank’s ‘All of the Above’ Approach to Energy in Poor Countries Is a Welcome Change,” Center for Global Development, April 18, 2025, https://www.cgdev.org/blog/world-banks-all-above-approach-energy-poor-countries-welcome-change.

14. David Manley, A. Furnaro, and Patrick Heller, “Riskier Bets, Smaller Pockets: How National Oil Companies Are Spending Public Money amid the Energy Transition,” Natural Resource Governance Institute, November 28, 2023, https://resourcegovernance.org/publications/riskier-bets-smaller-pockets-national-oil-companies-public-money-energy-transition.

15. Carbon Tracker Initiative, PetroStates of Decline: Oil and Gas Producers Face Growing Fiscal Risks as the Energy Transition Unfolds, December 1, 2023, https://carbontracker.org/reports/petrostates-of-decline.

16. Aaron Sayne, Framework for Countries Evaluating Gas-to-Power Pathways: Goal 1: Navigating the Energy Transition and Climate Crisis (Natural Resource Governance Institute, September 2022), https://resourcegovernance.org/sites/default/files/documents/gas_to_power_goal_1_navigating_the_energy_transition_and_climate_crisis_0.pdf.

17. Natural Resource Governance Institute, International Public Finance for Gas and Renewable Power in Africa: What is available?, September 2025, https://resourcegovernance.org/sites/default/files/2025-12/NRGI_PPT_International-public-finance.pdf.

18. World Bank, “World Bank Group Statement on the Nigeria Development Update,” April 9, 2026, https://www.worldbank.org/en/news/statement/2026/04/09/world-bank-group-statement-on-the-nigeria-development-update; O. Vallée, “La Banque mondiale n’est plus crédible,” Réveil de Caliban, April 11, 2026, https://oliviervallee.substack.com/p/la-banque-mondiale-nest-plus-credible.

19. Daan Walter, Sam Butler-Sloss, and Kingsmill Bond, The Electrotech Revolution: The Shape of Things to Come (Ember, September 2025), https://ember-energy.org/latest-insights/the-electrotech-revolution/.

20. International Monetary Fund, Energy Subsidy Reform in Sub-Saharan Africa: Experiences and Lessons (IMF, 2013); World Bank Group, Global Landscape of Fuel Subsidies & Price Controls (World Bank, April 2025).

21. Kingsley Jeremiah, “Nigeria, Africa starve local refineries, export 1.4b barrels crude”, The Guardian Nigeria, April 8, 2025.

22. Ver Femi Asu and Kanika Saigal, “Dangote vs the NNPC: The power struggle behind the refinery”, The Africa Report, March 3, 2025.

23. Tony Hodges, Angola: From Afro-Stalinism to Petro-Diamond Capitalism (Oxford and Bloomington, IN: James Currey and Indiana University Press, 2001), p. 129.

24. Economist Intelligence Unit, “Construction of Soyo Refinery Begins,” June 11, 2015.

25. Africa Energy Intelligence, “Why Is Lourenço Desperate to Hold On to Cabinda Refinery Mirage?,” July 17, 2018.

26. Kelly Norways, “Angola inaugurates first refinery newbuild in 50 years”, S&P Global, 3 September 2025, consultado em 14 January 2026, https://www.spglobal.com/energy/en/news-research/latest-news/refined-products/090325-angola-inaugurates-first-refinery-newbuild-in-50-years

27. César Esteves, “Refinaria do Lobito começa a funcionar no próximo ano”, Jornal de Angola, 14 January 2026.

28. Faustino Diogo and José Gonga, “Refinaria do Soyo continua em banho-maria enquanto Governo “cozinha” solução”, Expansão, 8 September 2025.

29. Sonangol, Refining Sector Overview: Existing Framework and Development Plan (Petrochemical and Refining Sonangol Business Unit, March 2022); IRDP, Relatório sobre os Combustíveis 2023 (Luanda: Instituto Regulador dos Derivados de Petróleo, March 2024).

30. On the benefits granted to the Cabinda refinery, see Sonangol, SNL Jornal Pacaça 67, September 2025, https://www.sonangol.co.ao/wp-content/uploads/2025/09/SNL-Jornal-Pacac%CC%A7a-67-ENG.pdf; Presidência da República de Angola, Decreto Legislativo Presidencial n.º 3/21, 18 June 2021, https://lex.ao/docs/presidente-da-republica/2021/decreto-legislativo-presidencial-n-o-3-21-de-18-de-junho/; Joaquim José Reis, “Sonangol ‘Saca’ 4,8 Mil Milhões USD ao Banco Chinês que é o Maior Credor Angolano”, Expansão, 3 February 2025.

31. Miguel Gomes, “Angola’s state oil firm Sonangol seeks $4.8 billion loan from China for refinery”, Reuters, February 25, 2026.

32. Africa Energy Portal, “Uganda Gov’t Signs Fresh Deals for $4bn Refinery,” November 20, 2025, https://africa-energy-portal.org/news/uganda-govt-signs-fresh-deals-4bn-refinery.

33. Uganda National Oil Company, “The Uganda Refinery Project,” n.d., https://www.unoc.co.ug/midstream/the-uganda-refinery-project/.

34. Africa Confidential, “Museveni’s $4 Billion Refinery Threatens East African Oil Pipeline,” May 14, 2025.

35. Uganda National Oil Company, “Kabalega Industrial Park,” n.d., https://www.unoc.co.ug/midstream/kabaale-industry-park/.

36. Petrosen, “Projet de Construction d’une Usine d’Urée,” Groupe Petrosen, May 23, 2024, https://www.petrosen.sn/projet-de-construction-dune-usine-duree/; Reuters, “Senegal Aims to Start Construction of New Refinery Next Year,” October 2, 2025, https://www.reuters.com/business/energy/senegal-aims-start-construction-new-refinery-next-year-2025-10-02/

37. Ministry of Planning and Territorial Development, National Development Plan 2013-2017, Luanda, December 2012.

38. Uche Usim, “Ogidigben Gas Industrial Park Secures $24.6bn Chinese Deal,” The Sun Nigeria, January 19, 2026, https://thesun.ng/ogidigben-gas-industrial-park-secures-24-6bn-chinese-deal/.

39. Africa Policy Research Institute, “Nigeria’s Natural Gas and Africa’s Sustainable Industrialization,” November 26, 2025, https://afripoli.org/nigerias-natural-gas-and-africas-sustainable-industrialization.

40. Victor Cariou, “Avec son « Petroleum Hub », le Ghana se rêve en premier raffineur d’Afrique de l’Ouest”, Le Monde, October 23, 2024.

41. Reuters, “Ghana Begins Construction of $12 Bln Petroleum Hub,” August 20, 2024, https://www.reuters.com/world/africa/ghana-begins-construction-12-bln-petroleum-hub-2024-08-20/.

42. International Energy Agency, Oil 2025: Analysis and Forecast to 2030 (IEA, 2025).

43. Mathias Larsen and Joachim Peter Tilsted, “The future of fossil fuels, chemicals, and feedstocks: Outlining a research agenda on the role of China in the global petrochemical industry”, Energy Research & Social Science, 118 (2024).

44. Kelly Norways, “Africa’s Refining Resurgence on Course Despite Margin Risk,” S&P Global, November 20, 2024, https://www.spglobal.com/commodity-insights/en/news-research/latest-news/crude-oil/112024-africas-refining-resurgence-on-course-despite-margin-risk; African Energy Chamber, The State of African Energy: 2026 Outlook Report (2026).

45. bp, Statistical Review of World Energy 2021; Energy Institute, 2025 Statistical Review of World Energy.

46. IEA, Financing Electricity Access in Africa (Paris: International Energy Agency, 2025).

47. Jyhjong Hwang (2021), “An Offer You Can Refuse: A Host Country’s Strategic Allocation of Development Financing”, Daedalus, 150(4), 194-219.

48. African Energy Commission, Electricity Generation in Africa from Fossil Fuels (AFREC, July 2023).

49. Ministère du Pétrole et des Énergies, “Note Synthétique : Stratégie « Gas to Power »” (Dakar: December 2018).

50. MIREMPET, Plano Director do Gás Natural (Luanda: Ministério dos Recursos Minerais, Petróleo e Gás, 2025).

51. NJ Ayuk, “The Surge in Gas Production and Africa’s Path to Economic Transformation”, African Energy Chamber, December 2, 2025, https://energychamber.org/the-surge-in-gas-production-and-africas-path-to-economic-transformation/

52. Ibid.

53. Papa Daouda Diene et al., Senegal’s Gas-to-Power Ambitions: Securing Scale and Sustainability (Natural Resource Governance Institute, June 2024).

54. Ibid.; Natural Resource Governance Institute, “How the Nigerian Government Can Right-Size Its Gas Ambitions for Economic Development,” 2 February, 2024., https://resourcegovernance.org/articles/how-nigerian-government-can-right-size-its-gas-ambitions-economic-development.

55. See, for example, Laura Carvalho, “The Hormuz Crisis and the Fate of the Global South”, Project Syndicate, 14 April 2026, https://www.project-syndicate.org/commentary/global-south-hormuz-crisis-opportunity-to-accelerate-economic-transition-by-laura-carvalho-2026-04

56. On the differing views of African and European policymakers on energy, see Sarah Logan and Maddalena Procopio, “Carbon Bargain: How Europe Can Adapt to Africa’s New Energy Alliances”, European Council on Foreign Relations, 29 January 2026, https://ecfr.eu/publication/carbon-bargain-how-europe-can-adapt-to-africas-new-energy-alliances/.

57. See, in particular, Alexandra Gillies, Marc Guéniat and Lorenz Kummer, Big Spenders: Swiss Trading Companies, African Oil and the Risks of Opacity (The Berne Declaration and NRGI, July 2014); and Douglas Porter and Catherine Anderson, Illicit Financial Flows in Oil and Gas Commodity Trade: Experience, Lessons and Proposals (Paris: OECD, 2021).

58. Isaac Anyaogu, “Nigeria’s richest man Dangote escalates oil fight with regulator, seeks corruption probe”, Reuters, December 15, 2025.

59. The Berne Declaration, Trafigura’s Business in Angola (2013), https://www.publiceye.ch/fileadmin/doc/Rohstoffe/2013_PublicEye_Trafiguras_Business_in_Angola_EN_Report.pdf.

60. Nicholas Shaxson, Oil and Capital Flight: The Case of Angola, PERI Working Paper Series: Capital Flight from Africa (University of Massachusetts Amherst, January 2021).

61. Rafael Marques de Morais, “O golpe da Sonangol e a crise dos combustíveis à vista”, Maka Angola, July 18, 2016.

62. See, for example, “Sonangol retoma abastecimento de combustível”, Expansão, 9 July 2014.

63. “Dificuldades no acesso a divisas pela Sonangol leva a escassez de combustíveis em Angola”, Diário de Notícias, May 4, 2019.

64. João Armando, “Terminal da Barra do Dande pronto 13 anos depois da sua apresentação”, Expansão, February 17, 2025.

65. Neil Hum and David Sheppard, “Angola oil overhaul tests ties with Trafigura”, Financial Times, Sep. 22, 2016; “The Dos Santos-Trafigura era bows out to Lourenco-Total era”, Africa Energy Intelligence, Oct. 2, 2018.

66. Zimbabwe provides a particularly striking example. See “How a Zimbabwe Tycoon Made a Fortune from a Trafigura Partnership and Spiralling National Debt”, OCCRP, 13 October 2021, https://www.occrp.org/en/investigation/how-a-zimbabwe-tycoon-made-a-fortune-from-a-trafigura-partnership-and-spiralling-national-debt

67. Mohamed Adow, “Middle East turmoil Is Africa’s wake-up call on oil”, Power Shift Africa, 2026, https://www.powershiftafrica.org/in-the-news/middle-east-turmoil-is-africas-wake-up-call-on-oil

68. Isaac Anyaogu, “Nigeria plans petroleum products stockpile to counter global supply shocks”, Reuters, April 15, 2025.

69. “Africa’s Energy Security Challenge is No Longer About Supply”, Invest in African Energy, March 27, 2026, https://invest-africa-energy.com/news/africas-energy-security-challenge-longer-supply

70. Ver Masami Kojima, Petroleum Markets in Sub-Saharan Africa: Analysis and Assessment of 12 Countries (Washington, DC: World Bank, 2010).

71. Shynia Hanaoka et al., “Performance of cross-border corridors in East Africa considering multiple stakeholders”, Transport Policy, 81, 2019, pp. 117-126.

72. Northern Corridor Transit and Transport Coordination Authority (NCTTCA), Strategic Plan for the Period 2022–2026 (Kigali: NCTTCA, 2022).

73. “Kenya and Uganda resolve oil import row, Uganda says”, Reuters, March 28, 2024.

74. Oluwadamilare Adeyemi et al., “West African Gas Pipeline Project: Law, Practice and Machinery”, International Journal of Comparative Law and Legal Philosophy, 5(1), 2023.

75. “Africa Must Refine, Baby, Refine: As Global Supply Disruptions Expose Need for Downstream Expansion”, African Energy Chamber, April 14, 2026, https://africanenergychamber.africa-newsroom.com/press/african-energy-chamber-africa-must-refine-baby-refine-as-global-supply-disruptions-expose-need-for-downstream-expansion?lang=en.

76. See also coverage in The Economist, “How to get African oil out of the ground without Western lenders: Go local, woo traders or head east”, 30 November 2023.

77. Nicolas Lippolis, “Sustainable Financial Taxonomies amid Geoeconomic Fragmentation,” Substack, March 26, 2026, https://cefd.substack.com/p/sustainable-financial-taxonomies-amid-geoeconomic-fragmentation.

78. OECD, Developing Sustainable Finance Definitions and Taxonomies (Paris: OECD, 2020).

79. For an example of a similar proposal, see Kenya’s National Energy Compact 2025-2030: https://thedocs.worldbank.org/en/doc/69843ca047603c8c4e993d2ff997f555-0010012025/original/Kenya-National-Energy-Compact-Mission-300.pdf

80. World Bank and IMF, Debt for Development Swaps: An Approach Framework (Washington, DC: World Bank and International Monetary Fund, 2024).

81. For an incisive critique, see Adam Tooze, “Chartbook 267: JET-P: The ‘Paper Tigers’ of Western Climate Geopolitics”, Chartbook, 22 February 2024, https://adamtooze.substack.com/p/chartbook-267-jet-p-the-paper-tigers.

82. Annika Seiler, Hannah Brown and Samuel Matthews, “The JETPs of South Africa and Indonesia: A Blueprint for the Move Away from Coal?”, CGD Policy Paper 302 (Washington, DC: Center for Global Development, 2023); Indri Dwi Apriliyanti, Diwangkara Bagus Nugraha and Indra Overland, “Explaining Indonesia’s failed energy transition: Mapping power and support for decarbonization among government institutions and actors”, Energy Research & Social Science, 135, 2026.

83. Harry Verhoeven and Gautam Jain, Africa’s Climate Finance Problem: African Sovereigns, Green Bonds, and Climate Action, Economic Trends (10) (Abu Dhabi: TRENDS Research & Advisory, September 2024).

84. Anahí Wiedenbrug, Strengthening the Foundations for Scalable Sustainability-Linked Sovereign Debt, IISD Policy Report (Winnipeg: International Institute for Sustainable Development, 2025).

85. See Archie Gilmour et al., Country Platforms in the context of rising sovereign debt levels (London: ODI Global, 2025).

86. Archie Gilmour, Josué Tanaka and Sarah Colenbrander, Designing and Governing Country Platforms: What role for MDBs? (London: ODI, October 2024); Archie Gilmour et al., Country Platforms in the context of rising sovereign debt levels (London: ODI Global, 2025).

87. Bastien Bedossa et al., Planning and Implementing the Climate and Development Transformation: Country Platforms as Enablers (Coalition for Capacity for Climate Action and Finance for Development Lab, 2025).

88. Ver Sam Hickey (ed.), Pockets of Effectiveness and the Politics of State-Building & Development in Africa (Oxford: Oxford University Press, 2023).

89. For an overview, see Shanthi Divakaran et al., Strategic Investment Funds: Establishment and Operations (Washington, DC: World Bank, 2022).

90. African Climate Foundation, “A New Chapter for Africa’s Energy Transition: Launching the REEF,” October 13, 2025, https://africanclimatefoundation.org/blog/a-new-chapter-for-africas-energy-transition-the-launch-of-the-renewable-energy-and-energy-efficiency-fund-reef/.

91. FONSIS, “Roundtable Discussion on Financing the Senegal Green Energy Fund: FONSIS Launches an Energy Transition Accelerator,” October 9, 2025, https://www.fonsis.org/en/table-ronde-reef/.

92. Nigeria Sovereign Investment Authority, Nigeria Infrastructure Fund Overview, n.d.; Nigeria Sovereign Investment Authority, Annual Report (2023).

93. M. Goosen, “Nigeria Launches $2B Climate Fund to Accelerate Energy Transition,” Energy Capital & Power, January 19, 2026, https://energycapitalpower.com/nigeria-launches-2b-climate-fund-to-accelerate-energy-transition/.

94. Divakaran et al., op. cit.

95. OECD, The Role of Sovereign and Strategic Investment Funds in the Low-carbon Transition (Paris: OECD, 2020).

96. Ibid.

97. Some principles on how to make pockets of effectiveness work in practice are outlined in Nicolas Lippolis, “‘Pockets of Effectiveness’ and Institutional Structures for Industrial Policy in Uganda”, EPN Note (Oxford: Centre for the Study of African Economies and Blavatnik School of Government, 15 July 2024).

98. Nicolas Lippolis and Ricardo Kotz, “Geoeconomics of Transition (Ed. 1),” Substack, January 15, 2026, https://cefd.substack.com/p/geoeconomics-of-transition-ed-1-back.

99. Akshat Rathi, “How Fossil Fuel Disruptions Lead to Booms in Solar and Batteries”, Bloomberg, March 5, 2026.