CEFD China-Latin America Cooperation Policy Paper Series

Ricardo Lopes Kotz

Abstract

By linking climate objectives to industrial competitiveness and technological upgrading, electric vehicles (EVs) have become strategic for the global energy transition, this study analyzes China–Brazil cooperation in electromobility, assessing whether Chinese foreign direct investment (FDI) supports upgrading and innovation in Brazil, or risks reproducing new forms of dependency within value chains. Drawing on a political economy approach, this study examines Chinese investment patterns, financing mechanisms, and industrial policies, with particular attention to financing mechanisms and technological cooperation, while also focusing on key cases such as BYD and Great Wall Motors. The study finds that, while Chinese investments have expanded manufacturing plants in Brazil, this is a recent phenomenon, whose developmental impacts are yet to unfold. Without deliberate institutional alignment, Brazil’s risks remain concentrated in downstream assembly and upstream resource extraction, instead of developing industrial capabilities closely related to technological upgrading, which tend to be concentrated in the mid-stream segments of the EVs value chain. The paper concludes with policy recommendations to ensure that China–Brazil cooperation supports green re-industrialization by embedding itself in long-term industrial and innovation strategies.

1. Introduction

Brazil is the largest economy in Latin America and its relative institutional stability and openness to innovation make it an attractive market for the diffusion of new technologies. Apart from increased trade relations, the country has seen a steady rise in Chinese foreign direct investment (FDI) since 2001, initially directed towards the oil, power, and agricultural sectors. More recently, Chinese investment has moved into renewables, IT, and manufacturing. However, the relationship remains heavily lopsided; while China has been advancing to the technological frontier in different segments of industry, Brazil has found it hard to do the same, as the country continues to export commodities such as soybeans, crude oil, iron ore, and beef (OEC-MIT 2025).

Despite being the largest net emitter of CO2 and other pollutants, China is also a global leader in renewable energy technologies, including solar, wind, ion-lithium batteries, and electric vehicles (IEA 2025). To compete in an energy transition increasingly shaped by “geoeconomics” (Meckling 2025), it is vital for countries to be able to develop proprietary clean energy technologies. This study thus asks the following question: to what extent do Chinese investments in Brazil contribute to upgrading and innovation capabilities? And how can Brazil capitalize on inward Chinese financing and technology to develop its battery and electric vehicle sectors?

This paper argues that the key to achieving this goal is developing coherent industrial policy frameworks that can use foreign investment as a springboard for the gradual construction of domestic capabilities. This requires coordinating across innovation policies, domestic regulation, and development finance instruments. In the absence of such coordination, FDI risks reproducing economic asymmetries, confining Brazil to downstream assembly and upstream resource extraction under the guise of green development.

The developmental impact of China–Brazil cooperation in electric vehicles and batteries hinges on state capacity and the strength of domestic institutions. FDI can bring capital, technology, and productive capabilities, but its benefits are never automatic. Without effective institutional embedding, foreign firms may operate as enclaves oriented primarily toward export markets or the extraction of local resources, with limited spillovers to the broader economy.

Targeted financing instruments, sector-specific industrial policies, and robust innovation mechanisms play central roles in mitigating these risks. By shaping investment incentives, lowering technological and financial risks, and fostering linkages with domestic firms, research institutions, and suppliers, these mechanisms enable FDI to be absorbed into the local economy. Foreign investment can thereby strengthen learning processes, upgrade productive capabilities, and anchor foreign investment in long-term development objectives.Instrumentos de financiamento direcionados, políticas industriais específicas para o setor e mecanismos consistentes de inovação desempenham papel central na mitigação desses riscos. Ao moldar incentivos para o investimento, reduzir riscos tecnológicos e financeiros e promover conexões com empresas nacionais, instituições de pesquisa e fornecedores locais, esses mecanismos permitem que o IDE seja efetivamente absorvido pela economia doméstica. Dessa forma, o investimento estrangeiro pode fortalecer processos de aprendizado, promover o adensamento tecnológico e ancorar-se em objetivos de desenvolvimento de longo prazo.

The rest of this paper is structured as follows. The first section delineates the main steps in the electric vehicles value chain, highlighting the key nodes of value creation. The second section examines Chinese foreign direct investment in Brazil’s electromobility and batteries, with particular attention to the cases of key firms such as BYD and Great Wall Motors. The following section analyses the financing and regulatory dimensions of this cooperation, focusing on the roles of the Brazilian National Development Bank (BNDES), industrial policy instruments, and recent regulatory developments. The fourth section explores innovation mechanisms and technological cooperation, and assesses their potential and limitations in fostering Brazil’s domestic capabilities. The next section presents policy recommendations aimed at strengthening Brazil’s position in the electromobility value chain. The final section synthesizes the main findings and discusses the conditions under which China–Brazil cooperation can support green reindustrialization rather than reinforcing structural dependency.

2. Steps in the electric vehicles value chain

The electric vehicle (EV) value chain is divided into upstream, midstream, and downstream segments, encompassing the sequential transformation of raw materials into assembled vehicles that are ready for commercialization.

Upstream activities involve raw material extraction and preliminary processing, whereas midstream core components are those that account for a significant portion of end-product value, such as batteries and powertrains. Downstream activities consist of final assembly, testing, distribution, and post-sale support.

This framework is valuable for understanding the different steps involved in the industrial process, the value added in each step, and possible bottlenecks within the EV ecosystem (Nazir and Mubarik 2026). The following subsections will describe in greater detail each of these three steps in the EV value chain.

2.1 Upstream: Critical minerals and inputs

Upstream operations initiate the value chain by extracting battery-grade minerals including lithium, cobalt, nickel, graphite, and rare earth elements. The subsequent value-added steps entail energy-intensive refining and smelting to yield high-purity precursors. Depending on how these processes are conducted, they can be energy- and water-intensive and can produce carbon emissions. Supply chain traceability and regulatory standards are important for mitigating production-related risks (Nazir and Mubarik 2026).

China is responsible for refining approximately 60% of the world’s lithium and cobalt used as production inputs, and Chinese firms have accumulated an estimated US$41.5 billion in outward FDI stock at this stage (Rhodium Group 2025). Brazil’s mineral base – including the lithium found in Minas Gerais’ Vale do Jequitinhonha, as well as nickel, manganese, graphite potential, and other inputs – creates an opportunity to negotiate investment packages that link upstream supply to other parts of the value chain, thus reducing the risk of Brazil remaining a commodity supplier while importing high value-added components.

Here, the policy challenge is to attract investment that builds processing, refining, and precursor material capacity, and not only extraction. In this regard, Brazil is currently engaging with the United States and the European Union in an effort to diversify sources of investment in critical minerals and avoid excessive reliance on any single source of FDI. The Brazilian Ministry of Mines and Energy has also initiated studies to develop a national strategy and industrial policy for developing the rare earths sector in the country (MME 2026). Despite holding the second largest reserves of rare earths after China and produces very small amounts of these minerals and the magnets derived from them (MME 2026).

2.2 Midstream: Processing, batteries, and cell-to-pack integration

Midstream processes aggregate refined inputs into electrochemical cells, modules, and packs via cathode/anode synthesis, electrolyte formulation, and cell assembly. These industrial processes have significant economies of scale that are frequently leveraged through mega-factories. Qualified suppliers fabricate components, such as electric motors, inverters, and thermal management systems.

With increasing demand across various markets, firms such as BYD have resorted to vertical integration strategies to ensure the quality of midstream activities, thus displacing their production near end consumer markets. The midstream segment constitutes the centerpiece of China’s overseas expansion in the EVs value chain. The stock of Chinese FDI in this segment amounts to approximately US$75.1 billion, most of which is located in Europe and North America. Batteries are the strategic core of EV and correspond to a large share of the value of the final good (Rhodium Group 2025).

Even when cells remain imported, pack assembly and integration – including cell-to-pack, battery management systems, and thermal control – can become entry points for domestic learning and supplier upgrading. Policy attention to battery ecosystems also converges with grid storage needs. There are opportunities for cross-sectoral spillovers in Chinese firms’ potential participation in Brazilian energy storage auctions (Maisonnave and Rathi 2026), since storage markets can support scale and learning in battery-related capabilities.

However, barriers to entry remain high due to the need for large investments and low profit margins.

2.3 Downstream: montagem, manufatura final e comercialização

Downstream activities culminate in the OEM vehicle platform, where battery systems are integrated with hardware and software and prepared for market deployment. Value creation increasingly extends beyond manufacturing into charging infrastructure and post-sale services, including digital monitoring and end-of-life strategies that redirect degraded batteries toward second-life applications (Nazir and Mubarik 2026).

Local assembly can thus generate employment and supplier opportunities, but development spillovers are substantially higher when investments include localized engineering, testing, product adaptation, and industrial services. The stock of Chinese investment in downstream activities totals US$26.8 billion worldwide (Rhodium Group 2025).

Chinese investment in midstream activities is predominantly concentrated in Europe and the United States, where access to advanced technologies and large consumer markets provides strong incentives for foreign direct investment (FDI). In contrast, investment in Latin America has focused on upstream sectors, such as lithium and copper extraction along the Pacific coast, with a limited number of downstream initiatives linked to EV assembly and commercialization, mostly in Brazil. The latter are discussed in greater detail in the next section, which surveys the landscape of electromobility investment in Brazil.

3. Chinese FDI in EVs and batteries

3.1 Overall patterns

Chinese investment in Brazil is growing as China consolidates its leading position across global EV and battery value chains. A model grounded in long-term industrial planning, coordinated public–private investment, and a dense innovation ecosystem has enabled Chinese firms to internalize key segments of the value chain – from battery production and power electronics to vehicle assembly – while progressively moving toward higher value-added activities. Brazil presents a distinct and complementary set of structural advantages, including a large domestic automotive market, a predominantly renewable electricity mix, and substantial endowments of critical minerals relevant to battery technologies. These assets are reinforced by the presence of public development institutions and industrial policy instruments in the region.

The growing presence of Chinese firms in Brazil’s electromobility ecosystem reflects the broader reconfiguration of the value chain following the COVID-19 pandemic, as China has emerged both as a manufacturing hub and a major source of capital and technology. However, this expansion raises a critical question for development policy: under what conditions can Chinese foreign direct investment contribute to structural transformation and the upgrading of productive capabilities in host economies? Rather than assuming automatic spillovers from FDI, the developmental impact of Chinese investment depends on how it is embedded in the local institutional frameworks, financing arrangements, and innovation systems.

Brazil offers a crucial case for assessing whether and how South–South cooperation in electric mobility can move beyond market access and assembly operations in the Global South. Critical mineral projects under electromobility firms such as BYD are mentioned in the table below, seeing as these resources are important inputs for batteries, and evidence points to Chinese firms’ interest in investing in mineral resources to integrate their value chains in South America (CEBC 2025). The table below summarizes the main Chinese FDI projects in this sector in Brazil.

Table 1: Major Chinese FDI projects in electromobility, critical minerals, and batteries in Brazil between 2015-2025

| Project / Asset | Chinese firm | Year | Sector | Investment (USD million) | Mode of Entry |

| Chery Engine Plant and expansion | Chery | 2012/2015 | Manufacturing | 400 + 8 | Greenfield/Brownfield |

| Electric bus assembly factory | BYD | 2015 | Manufacturing | 150 | Greenfield |

| Automobile assembly factory | Chery | 2015 | Manufacturing | 1 | Greenfield |

| Solar panel factory | BYD | 2017 | Manufacturing | 47 | Greenfield |

| Automotive parts factory | Yapp Automotive Systems | 2019 | Manufacturing | 24 | Greenfield |

| Fábrica para a montagem de baterias elétricas | BYD | 2020 | Manufatura/Energia | 3 | Greenfield |

| Acquisition of Daimler factory | Great Wall Motors | 2021 | Manufacturing | 120 | Acquisition |

| Acquisition of Poliron | YOFC | 2021 | Manufacturing | 12 | Acquisition |

| Camacari Industrial complex | BYD | 2023 | Manufacturing | 620 | Acquisition |

| BYD’s Acquisition of Mining rights in Lithium mining in Minas Gerais state | BYD | 2023 | Mining | 4 | Acquisition |

| Acquisition of Mineração Vale Verde | Baiyin | 2024 | Mining | 420 | Acquisition |

| Acquisition of Mineração Taboca | China Nonferrous Metal Mining Group | 2024 | Mining | 340 | Acquisition |

| São Paulo–Campinas TIC & Jundiaí–Campinas TIM railways | CRRC | 2024 | Infrastructure | 2600 | Construction project (electricity fueled) |

| Acquisition of engine manufacturing plant from Horse Powertrain (JV between Geely, Renault & Saudi Aramco) in Parana State | Geely | 2024 | Manufacturing | 546 | Acquisition/ Joint venture |

| Acquisition of 26.4% of Renault’s Brazil operations, forming a Joint Venture investing in an EV Plant in Parana state) | Geely | 2025 | Manufacturing | 730 | Acquisition/ Joint venture |

Source: Elaborated by the author based on data compiled by Red-America Latina China (2025) on Chinese FDI in Latin American countries between 2000-2024.

Chinese FDI in Brazil is not limited to exporting vehicles but is part of a broader strategy aimed at securing a competitive position in a large market by building local manufacturing facilities and potentially integrating these facilities with other steps of the value chain, even if often using parts and components that are still produced in China. Estimates vary but, overall, China’s stock of FDI in the Brazilian market totals circa US$ 73-76 billion between 2000-2024, making it an important player across different sectors (AEI 2025; Red America Latina-China 2025).

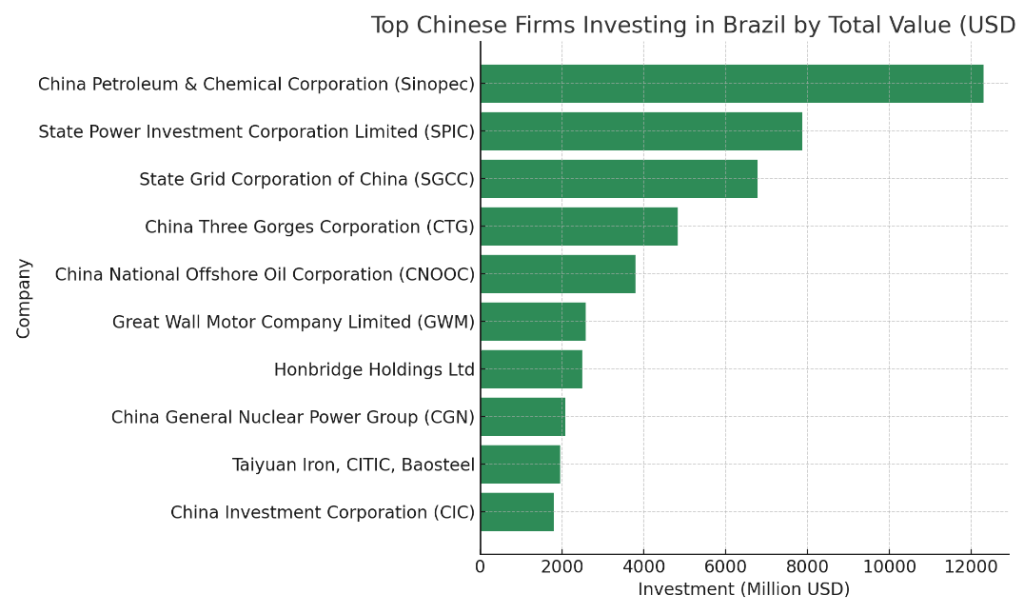

As shown by Figure 1, the top five Chinese investors in Brazil are in the oil and power sectors. Great Wall Motors comes in in sixth place, ahead of other mining and power interests. It thus stands out as the sole automotive sector representative among China’s top investors in Brazil.

Figure 1: Top Chinese firms investing in Brazil by value (FDI) between 2000-2024:

Source: Elaborated by the author based on data compiled by Red-America Latina China (2025) on Chinese FDI in Latin American countries between 2000-2024.

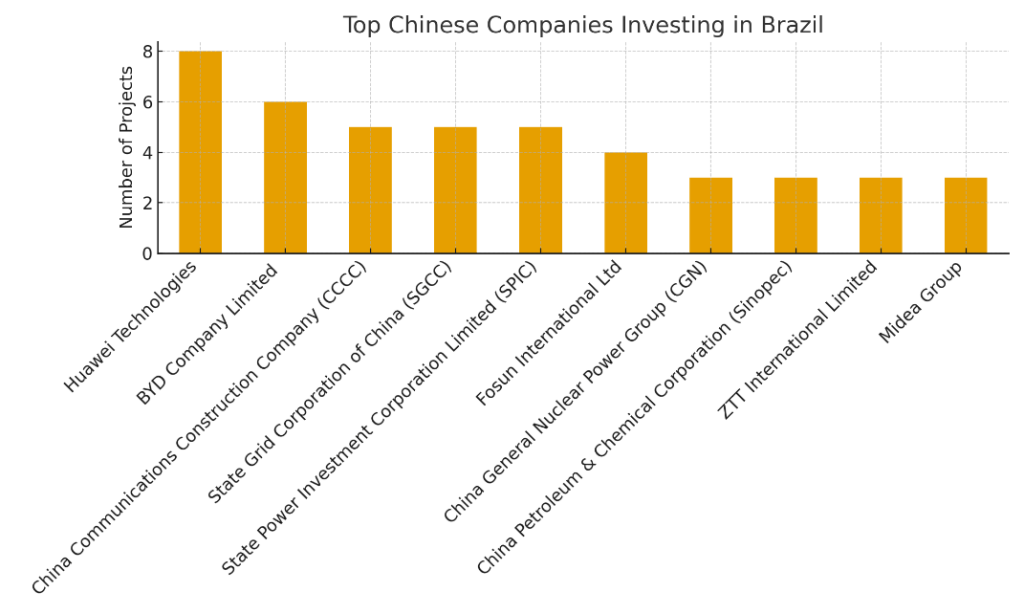

In contrast to the total investment figures, Figure 2 shows that when counted in terms of total projects, there is greater representation of telecommunications firms. BYD is the only EV producer to make the list, with a total of six direct investment projects in Brazil. The data thus suggests that EV producers still make up a relatively minute proportion of total Chinese direct investment in Brazil.

Source: Elaborated by the author based on data compiled by Red-America Latina China (2025) on Chinese FDI in Latin American countries between 2000-2024.

Source: Elaborated by the author based on data compiled by Red-America Latina China (2025) on Chinese FDI in Latin American countries between 2000-2024.

3.2 The case of BYD

In terms of electromobility and batteries, BYD and Great Wall Motors are the main Chinese investors in electromobility and batteries in Brazil. BYD has developed a diversified manufacturing presence in the country. The Shenzhen-based producer’s Brazilian operations began in 2015 with the inauguration of a factory in Campinas, São Paulo, dedicated to the assembly of electric buses and chassis for urban transport systems. The same location later incorporated a photovoltaic module plant, inaugurated in 2017, aimed at supplying solar panels to the domestic clean-energy market. In parallel, BYD established a battery manufacturing facility in the Manaus Industrial Pole dedicated to the production of lithium iron phosphate batteries (BYD 2024; 2025). This plant is recognized as the first factory in Brazil specifically designed for the production of batteries for electric vehicles, reinforcing the firm’s vertical integration strategy.

By 2023, the firm expanded its production facilities in the country through large-scale manufacturing investments in Camaçari, Bahia. This project represents the company’s largest manufacturing venture outside Asia and has transformed a former Ford automotive complex into a major production hub for electric and hybrid vehicles. The total investment was estimated to be approximately US$ 620 million, showcasing the firm’s commitment to the Brazilian market (BYD 2025).

The Camaçari facility was officially inaugurated in October 2025 and began producing a range of passenger vehicles, including the locally assembled Dolphin Mini, as well as hybrid and plug-in hybrid models such as the Song Pro. The initial installed capacity is estimated to be 150,000 vehicles per year, with planned expansion phases that could increase the output to 300,000 units or more by the early 2030s. BYD has articulated the strategic objective of positioning Brazil as a regional export platform for Latin American markets. By late 2025, the plant had already reached a production milestone of approximately 20,000 vehicles and was operating on a two-shift basis, indicating a gradual scaling up of operations (BYD 2024; 2025; Ko 2025). Nevertheless, although production has formally commenced, full operational capacity may only be achieved by July 2026 because of construction delays and labor-related challenges. Beyond manufacturing, BYD has taken steps to build infrastructure by partnering with Raízen Power, through its Shell Recharge operations, to create 600 charging stations across major Brazilian cities (BYD 2024).

3.3 The case of Great Wall Motors

Great Wall Motors (GWM) is the other major Chinese EV investor in Brazil. GWM entered the Brazilian market by acquiring a Mercedes-Benz plant in Iracemápolis, São Paulo state, in 2021. The plant was previously owned by Daimler AG and closed in December 2020 owing to unfavorable market conditions. This acquisition allowed GWM to bypass bureaucratic procedures often associated with greenfield investments in Brazil while leveraging existing infrastructure to rapidly initiate operations. The facility was later expanded and reformed for EV production. The plant spans 1.2 million square meters, with 94,000 square meters of built-up area and an initial annual prod

uction capacity of 50,000 vehicles. Production capacity is scalable to 100,000 units and the plant is claimed to be generating over 1,000 direct jobs (Great Wall Motors 2024; 2025b).

The Iracemápolis plant prioritizes flexible hybrids and electric vehicles, starting with the HAVAL H6 GT SUV, followed by the HAVAL H9 SUV and POER P30 pickup truck, all featuring hybrid (HEV), plug-in hybrid (PHEV), flex-fuel (gasoline/ethanol), and diesel variants tailored to Brazil’s biofuel-dominant market with a flex engine. This localization feature aligns with Mercosur export quotas, enabling duty-free shipments to Argentina and Paraguay. The plant also has a Research & Development (R&D) center that focuses on flex-fuel innovations, regional adaptations, and supply chain integration (Great Wall Motors 2025a).

4. Financing mechanisms

4.1 The role of BNDES

BNDES has played a central role in shaping Brazil’s approach to energy transition and its nascent electric mobility ecosystem. BNDES operates not only as a provider of long-term credit, but also as a policy instrument through which the Brazilian state seeks to coordinate industrial upgrading, technological diffusion, and infrastructure expansion (Hochstetler 2021). In the context of low-carbon technologies, the bank’s financing strategies reflect a dual mandate: supporting decarbonization objectives aligned with Brazil’s climate commitments while simultaneously fostering domestic productive capabilities in strategic sectors (Vaz 2026).

Historically, BNDES financing for the automotive sector was oriented toward the conventional vehicle value chain, as Brazil occupied the 8th position among the largest automotive manufacturing countries and possessed the world’s 6th largest automotive consumer market in 2024 (Valor Economico, 2025). However, over the last decade, this orientation has progressively shifted toward electrification, energy efficiency, and innovation-intensive segments of the value chain. This transition occurred gradually and pragmatically rather than through abrupt substitution. BNDES has continued to finance internal combustion–related activities, where employment and export revenues remain relevant, but has increasingly incorporated conditionalities and incentives linked to technological upgrading, emissions reduction, and alignment with national industrial and environmental policy frameworks (Fundep 2025).

In the field of electric mobility, BNDES financing focuses less on consumer subsidies and more on the productive and infrastructural foundations of the sector. This includes credit lines and blended finance instruments aimed at vehicle manufacturing, component production, charging infrastructure, and innovation. By prioritizing long-term financing for capital-intensive investments, the bank addresses a key structural barrier to EV diffusion in Brazil: the high upfront costs associated with manufacturing retooling, supply chain adaptation, and grid integration. In this sense, BNDES acts as a de-risking agent, lowering the cost of capital for firms willing to invest in emerging technologies whose commercial returns may materialize only over extended time horizons (Sbardelotto et. Al. 2023; BNDES 2024).

In addition to vehicles and batteries, BNDES is a major financier of renewable energy generation, particularly wind, solar, and hydropower, as well as electricity transmission and distribution systems. From an institutional perspective, the bank has increasingly aligned its financing instruments with national industrial policies, including programs explicitly designed to foster green reindustrialization (BNDES 2023; 2025a).

A key mechanism through which BNDES has fostered green industrialization is the enforcement of local content requirements (LCRs) in the energy sector. The bank provides long-term loans at interest rates substantially below market levels, but access to this financing is conditional on compliance with strict localization targets, thereby compelling international manufacturers to establish local production facilities in Brazil to remain competitive. BNDES has also acted as a disciplinarian within the renewable energy industry, withdrawing support wherever loan conditions are not met. This approach effectively transformed access to finance into a powerful tool for fostering domestic manufacturing capabilities (Hochstetler 2021).

The bank’s role extends beyond domestic financing. BNDES also manages international climate finance instruments, including resources from the Amazon Fund, and proceeds from green bonds issued in international capital markets. These funds are subsequently channeled into energy transition sectors, including wind and solar infrastructure projects, reinforcing the bank’s position as an intermediary between global climate finance and national development priorities (Hochstetler 2021).

The developmental impact of BNDES’ financing for the electric vehicles and battery sectors remains contingent on several structural challenges. These include the limited scale of domestic demand for EVs relative to major global markets, persistent gaps in technological capabilities, and the strong competitive advantage of foreign firms – particularly Chinese – across critical segments of the value chain.

BNDES has played a catalytic role in advancing the decarbonization of urban mobility through electrification. In December 2024, it approved a disbursement of R$ 380 million from Brazil’s Climate Fund to support Curitiba’s procurement of 54 battery-electric buses and the installation of two charging stations under the New Program for Acceleration of Growth (PAC). This intervention helped expand Brazil’s still limited fleet of electric buses. The program aims to reach a total stock of 107,000 units, whose full renewal will require an estimated R$ 214 billion (US$ 41 billion) over a 13-year horizon.

In the battery segment, BNDES approved a 16-year, R$ 487 million (US$ 94 million), a 16-year development loan to Sigma Lithium in August 2024, to finance Phase 2 of the Grota do Cirilo project in Minas Gerais’ Lithium Valley. The project aims to strengthen Brazil’s incipient EV battery supply chain by increasing carbon-neutral lithium production to 540,000 tons per year (Fundep 2025; Neris 2025).

4.2 Electromobility-related industrial policies

Beyond the role played by BNDES, Brazil has introduced a series of laws, regulations and policy programs aimed at promoting the electromobility sector (Table 2).

The Mover industrial policy for the automotive sector was instituted in 2024, but it originated from the previous Rota 2030 policy, upgrading its scope and objectives. The policy seeks to promote a reduction in carbon emissions in the automotive sector through the adoption of new mobility technologies, such as electric vehicles, alternative propulsion systems – including biofuels, hydrogen, and other low-carbon alternatives – and higher environmental standards in manufacturing processes.

Through tax incentives and subsidized credit, Mover supports automakers and supply-chain firms undertaking R&D and innovation in sustainable mobility and green technologies, mobilizing up US$ 19 billion by 2028 (Office of the Presidency of Brazil 2024; 2025).

Table 2: Regulatory instruments and policies enacted by Brazil regarding electromobility (2020-2025):

| Year | Policy Name / Instrument | Policy Level | Policy Type | Key Measures & Objectives | Category | Source |

| 2020 | EVSE Building Requirements – São Paulo | Subnational (City of São Paulo) | Legislation | Mandates that new buildings prepare and plan for electric vehicle charging infrastructure (EVSE). | Infrastructure | City of São Paulo |

| 2021 | Deputies Bill No. 2156/2021 | National | Proposal | Establish | Taxation | Brazil’s Federal Government |

| 2022 | Senate Bill No. 403/2022 | National | Proposal | Proposes exemption from import tax for electric and hybrid vehicles to stimulate market adoption. | Taxation | Brazil’s Federal Government |

| 2023 | Resolution No. 532/2023 (CAMEX) | National | Regulation | Establishes the gradual reintroduction of import taxes on electric, hybrid, and plug-in hybrid vehicles. | Trade / Taxation | Brazil’s Federal Government |

| 2024- 2028 | National Green Mobility and Innovation Program – MOVER (Law 14.902/2024) | National | Legislation | Defines new automotive sector guidelines, fleet sustainability requirements, incentives for new technologies, up to R$ 19.3 billion in credits (2024–2028), and a National Fund for Industrial Development. | Industrial Policy / Innovation | Brazil’s Federal Government |

| 2025 | Regulation for recycling and battery reuse (PL 158/2025)Regulamentação para a reciclagem de Baterias (PL 158/2025) | National | Senate Bill | Made to regulate the extended responsibility of producers regarding the lifecycle of batteries, fostering reuse and recycling. | Instrumento de Política Industrial | Brazil’s Federal Government |

Source: Elaborated by the author based on MDIC (2025) and ANEEL (2025).

The main support measures foreseen by Mover include (Office of the Presidency of Brazil 2024; 2025):

- A provision of tax credits equivalent to 50 percent of research and development (R&D) spending for firms investing between 0.3 and 1.8 percent of their revenues on R&D in areas such as electric vehicle batteries, power electronics, or software.

- Tax credits rise up to 320 percent of what is spent on R&D when combined with bonuses linked to exports, frontier technologies, or the establishment of new production facilities.

- A technological production bonus whereby investments in advanced components, including electric motors and other high-value parts, generate tax credits that range from 12.5 to 25 percent of the amounts invested.

- A full rebate on import taxes for companies that transfer production lines to Brazil. Eligible companies are entitled to reductions in Corporate Income Tax (IRPJ) and the Social Contribution on Net Profits (CSLL) for products and systems produced and exported from Brazil.

- For automotive components not yet produced domestically, firms are required to contribute 2 percent of their import value to the National Fund for Industrial and Technological Development (FNDIT), which reinvests these resources through concessional loans aimed at fostering local production and supplier development.

Complementing this, the Nova Indústria Brasil (NIB) framework is a broad, encompassing mission-oriented policy launched in 2024, with the goal of promoting green industrialization in the country over the next ten years. The program was developed by the National Council for Industrial Development (CNDI), and project actions through 2033 with an initial R$300 billion (US$ 58 billion) in financing to be conceded by 2026, primarily via BNDES loans, subsidies, and public procurement preferences. It integrates fiscal, regulatory, and technological instruments to align industrial growth with global trends, such as decarbonization and digitalization (MDIC 2025). The 13 policy instruments deployed by the program include subsidized loans, non-reimbursable grants, tax credits, tech transfers, local content requirements, and public purchases that favor national goods.

Hiratuka (2022) affirms that Chinese foreign direct investment (FDI) can play an important role in helping Brazil move beyond natural resources, provided it is channeled into knowledge-intensive, technologically dynamic, and environmentally sustainable activities. The case of BYD illustrates the potential for a more development-oriented engagement pattern. Adopting a “Brazil-for-Brazil” strategy, the company established local production facilities for electric bus chassis, photovoltaic panels, and batteries in order to comply with domestic content requirements. This localization strategy enabled BYD to access financing instruments, such as FINAME from the Brazilian Development Bank (BNDES), which are crucial for competing in Brazil’s public procurement and transport markets (Hiratuka 2022). In this sense, industrial policy instruments and development finance have emerged as key mechanisms for embedding foreign investment into domestic productive structures.

5. Innovation mechanisms and technological cooperation

China’s experience with low-carbon policy design and technology deployment has often been more relevant to Brazil than models imported from advanced economies, reflecting shared development constraints and institutional realities. The creation of the China–Brazil Center for Climate Change and Energy Technology Innovation, officially endorsed by Presidents Lula da Silva and Hu Jintao in 2010, was the basis for bilateral cooperation in science and technology and coincided with broader coordination among emerging economies through the BASIC group. The Center provided a permanent institutional base for scientific collaboration, serving as a platform through which multiple sectoral cooperation efforts have been articulated and sustained over time. In 2015, cooperation was further expanded through the establishment of the China–Latin America Joint Laboratory on Clean Energy and Climate Change, which broadened the scope of collaboration beyond the bilateral level and positioned China–Brazil cooperation as a reference for the region (Lewis 2023).

Despite some achievements, particularly in the biofuels sector, technological cooperation between the two countries has also suffered from structural vulnerabilities. Economic downturns and shifts in political priorities in Brazil weakened institutional support after 2014, reducing China’s engagement. Moreover, commercial deployment faced obstacles stemming from incompatible market structures, as illustrated by the failure of wind power projects, owing to mismatches between Chinese expectations of guaranteed sales and Brazil’s auction-based electricity market (Lewis 2023).

More recently, BYD has invested approximately R$ 65 million (US$ 12.5 million) in photovoltaic R&D initiatives within Brazil, reinforcing its strategic emphasis on technological innovation in renewable energy. The company also built Latin America’s First Photovoltaic Corporate Laboratory, located in Campinas, with an initial investment of US$ 7 million. As the first corporate center in Latin America dedicated to the full-cycle testing and research of photovoltaic modules, it covers material analysis, module behavior under tropical conditions, and integration performance (BYD 2024; 2025).

BYD has also been active in the rollout of solar power infrastructure. A joint venture between the subsidiary BYD Energy and the Brazilian energy firm (but partly Shell-owned) Raízen has built nine photovoltaic plants, with a combined installed capacity of 26.5 MW. The partners also announced plans to install 600 charging stations across eight Brazilian capitals to stimulate demand in what remains an incipient EV market (BYD 2024). Yet progress has lagged behind expectations: by the end of 2024, only 50 high-power public chargers had been installed (BYD 2025).

Overall, the China–Brazil experience highlights both the potential and fragility of the South–South cooperation in low-carbon innovation. While such partnerships offer emerging economies greater control over supply chains and intellectual property, their sustainability depends on a stable political commitment, funding continuity, and institutional compatibility. From an innovation perspective, the EV and battery sectors are characterized by rapid technological change, cumulative learning processes, and strong complementarities between production and knowledge generation. This places an even greater premium on the institutional and policy consistency that has often proven elusive in Brazil.

6. Conclusion and policy implications

China–Brazil cooperation in electric vehicles and batteries sits at the intersection of climate goals and industrial development. As this policy paper has shown, up to now, Chinese FDI has made limited contributions to expanding manufacturing capacity in Brazil, as new firms have only recently begun entering the country and they still import many components from China. This is nonetheless an initial step that could lead to Brazil being more firmly embedded in global electromobility value chains.

However, the developmental outcomes of this engagement are not automatic. Without deliberate policy coordination and long-term institutional engagement, Brazil risks reproducing existing asymmetries, remaining concentrated in the downstream assembly of vehicles and upstream resource extraction, while higher value-added activities, technological learning, and standards remain concentrated in China, thus reproducing the logic of the North-South divide instead of generating a South-South common development framework. The evidence suggests that the decisive variable is not only the scale of Chinese investment per se but also the institutional frameworks and policies that govern financing, innovation, and value-chain integration.

Going forward, policy should prioritize the “missing middle” of the value chain – tooling, automation, electronics, industrial software, quality systems, and green certification – where spillovers are large and Brazilian firms remain weakly positioned. Strengthening these segments will require targeted industrial policy, including the development of specialized industrial parks and coordinated financing across national and subnational governments in partnership with lead firms. Aligning domestic institutions and mobilizing instruments such as MOVER, the NIB, and BNDES support around clear conditionalities will be central to this effort, particularly when combined with collaboration with universities and research centers. Over the medium-too long term, sustained investment in technical skills and workforce specialization will be indispensable.

If strategically managed, China–Brazil cooperation can support a reindustrialization effort that combines decarbonization with productive upgrading. However, if Brazil remains a passive recipient of FDI, Chinese capital may simply become another wave of investors interested in accessing local resources and the large market, which could reinforce path-dependency on commodity production; the difference is that it would now be termed within the label of the green economy and energy transition. The challenge for Brazil is to turn this cooperation into leverage and competitive capabilities, using the energy transition not only to reduce emissions but also to reshape its industrial future through clear long-term strategies, industrial and technology policies, and effective institutions.

7. References

American Enterprise Institute. (2025). Chinese global investment tracker. AEI.

Agência Nacional de Energia Elétrica. (2026). Biblioteca virtual da ANEEL. Governo Federal do Brasil. https://biblioteca.aneel.gov.br/

Banco Nacional de Desenvolvimento Econômico e Social. (2023). BNDES guidelines for climate change. BNDES.

Banco Nacional de Desenvolvimento Econômico e Social. (2024a). Programa prioritário BNDES Rota 2030: Descarbonização da mobilidade e da logística. BNDES.

Banco Nacional de Desenvolvimento Econômico e Social. (2024b, December 4). Com R$ 380 mi do Fundo Clima, BNDES financia aquisição de 54 ônibus elétricos em Curitiba. https://www.bndes.gov.br/wps/portal/site/home/imprensa/noticias/conteudo/com-r-380-mi-do-fundo-clima-bndes-financia-aquisicao-de-54-onibus-eletricos-em-curitiba

Banco Nacional de Desenvolvimento Econômico e Social. (2025a). Programa BNDES MOVER de descarbonização da mobilidade e logística. BNDES.

Banco Nacional de Desenvolvimento Econômico e Social. (2025b). Relatório anual e dados setoriais sobre financiamento à transição energética. BNDES.

BloombergNEF Intelligence Unit. (2025). China’s energy transition at a crossroads. BloombergNEF Insights. https://about.bnef.com/insights/clean-energy/chinas-energy-transition-at-a-crossroads

BYD. (2024). Innovation blueprint: BYD 2024. Liga Ventures. https://liga.ventures/insights/relatorios/innovation-blueprint-byd/

BYD Company Ltd. (2023). Global report 2024. BYD Global.

BYD Company Ltd. (2024, February 4). BYD and Raízen Power form a strategic partnership to boost sustainable electric mobility in Brazil. https://www.byd.com/us/news-list/BYD-Raizen-Power-Form-Strategic-Partnership-Boost-Sustainable-Electric-Mobility-Brazil

BYD Brasil. (2025). Relatório de sustentabilidade 2025 (Versão final). https://bydbrasil.com.br/wp-content/uploads/2025/08/BYD-Relatorio-de-Sustentabilidade-2025-Versao-final-portugues.pdf

BYD. (2025). Relatório anual e investimentos globais em eletromobilidade. BYD Auto.

Fundação de Desenvolvimento da Pesquisa. (2025). Instrumentos de financiamento e inovação industrial no Brasil. Fundep.

Government of Brazil. (2024, January 26). Brazil launches new industrial policy with development goals and measures up to 2033. Planalto. https://www.gov.br/planalto/en/latest-news/2024/01/brazil-launches-new-industrial-policy-with-development-goals-and-measures-up-to-2033

Great Wall Motors. (2024). GWM Brazil: Industrial strategy and localization roadmap. GWM.

Great Wall Motors. (2025a, July 4). GWM Brasil cresce 7 vezes mais que o mercado neste ano e lidera com o Haval H6 entre os híbridos. https://www.gwmmotors.com.br/pt/media-center/news/2025/gwm-brasil-cresce-7-vezes-mais-que-o-mercado-neste-ano-e-lidera-com-o-haval-h6-entre-os-hibridos

Great Wall Motors. (2025b, August 16). GWM Brazil plant officially opens with President Lula in attendance [Press release]. https://www.gwm-global.com/news/3403758.html

Hiratuka, C. (2022). Why Brazil sought Chinese investments to diversify its manufacturing economy. Carnegie Endowment for International Peace.

Hochstetler, K. (2020). Political economies of energy transition: Wind and solar power in Brazil and South Africa. Cambridge University Press.

International China–Latin America Center. (2025). Chinese foreign direct investment in Latin America and the Caribbean.

International Energy Agency. (n.d.). China country profile — Energy mix. Retrieved January 27, 2026, from https://www.iea.org/countries/china/energy-mix

Instituto Nacional de Pesquisas Espaciais. (n.d.). CBERS: Satélite Sino-Brasileiro de Recursos Terrestres. Governo do Brasil. https://www.gov.br/inpe/pt-br/programas/cbers

Investing.com. (2024, August 29). Sigma Lithium secures $92 million BNDES loan for new plant. https://www.investing.com/news/company-news/sigma-lithium-secures-92-million-bndes-loan-for-new-plant-93CH-3594015

Jenkins, R. (2015). Is Chinese competition causing deindustrialization in Brazil? Latin American Perspectives, 42(6), 42–63. https://doi.org/10.1177/0094582X15593553

Ko, P. (2025). How China is using Brazil to reshape power in the Americas. The Diplomat. https://thediplomat.com/2025/11/how-china-is-using-brazil-to-reshape-power-in-the-americas/

Lewis, J. I. (2023). Cooperating for the climate: Learning from international partnerships in China’s clean energy sector. MIT Press.

Maisonnave, F., & Rathi, A. (2026, January 23). Brazil is set for a battery boom. China is poised to benefit. Bloomberg.

Meckling, J. (2025). The geoeconomic turn in decarbonization. Nature, 645, 869–876. https://doi.org/10.1038/s41586-025-09416-x

Ministério da Indústria, Comércio Exterior e Serviços. (2024, May). Programa BNDES Rota 2030: Descarbonização da mobilidade e da logística [PDF]. https://www.gov.br/mdic/pt-br/assuntos/sdic/setor-automotivo/projetos-e-programas-prioritarios/programas-prioritarios-credenciados/ProgramaBNDESROTA2030DescarbonizaodaMobilidadeFOLHETO_13.05.2024.pdf

Ministry of Development, Industry, Commerce and Services of Brazil. (2025). Nova Indústria Brasil – Plano de Ação 2024–2026 (versão atualizada). MDIC/CNDI.

Ministério de Minas e Energia. (2026, January 22). MME inicia estudos para construção da Estratégia Nacional de Terras Raras. Governo do Brasil. https://www.gov.br/mme/pt-br/assuntos/noticias/mme-inicia-estudos-para-construcao-da-estrategia-nacional-de-terras-raras

Mubarik, M. S., Vilko, J., & Nazir, S. (Eds.). (2026). Electric vehicle supply chain management (1st ed.). Routledge.

Neris, A. (2025, October 30). ION Energia impulsiona BESS as a Service no Brasil e busca equipamentos nacionais. pv magazine Brasil. https://www.pv-magazine-brasil.com/2025/10/30/ion-energia-impulsiona-bess-as-a-service-no-brasil-e-busca-equipamentos-nacionais/

Observatory of Economic Complexity. (2025). Brazil (BRA) profile. OEC. Retrieved January 27, 2026, from https://oec.world/en/profile/country/bra

Red América Latina–China. (2025). Monitor de investimentos chineses na América Latina (2000–2024).

Rhodium Group. (2024). China’s global electric vehicle investments. Rhodium Group.

Rhodium Group. (2025). Database of Chinese global FDI in electric vehicles. Rhodium Group.

Sbardelotto, L. (2023). Regulatory challenges in the electromobility sector: An analysis of electric buses in Brazil. Energies, 16(8), 3510. https://doi.org/10.3390/en16083510

Sino-Brazilian High-Level Commission for Concertation and Cooperation (COSBAN). (2015–2021). Joint action plans and bilateral cooperation frameworks. Governments of Brazil and China.

Valor Econômico. (2025). Brasil consolida posição entre os maiores produtores automotivos globais. Valor Econômico.

Vaz, A. (2026). Development banks and the energy transition in emerging economies: The role of BNDES. Journal of Development Studies. (Forthcoming).